With five matchdays to go, Tottenham currently sit eighteenth in the EPL table, two points away from safety outside the relegation zone. While hard to imagine the unthinkable, it is a very realistic possibility that Spurs are playing next season in the Championship. To frame the financial impact of relegation, FootyFinance has prepared a hypothetical financial model for a Tottenham season spent in the Championship next year. The model assumes Tottenham will be promoted back to the EPL following one season in the Championship. Any additional seasons in the second tier will further erode financial metrics, driven by declining commercial appeal for sponsors, reduced matchday pricing power and attendance, and diminishing contribution from parachute payments. An overview of the financial drivers leading up to Tottenham’s relegation fight can be found here (Not Too Big to Fail – The Financial Drivers Behind Tottenham’s Unprecedented Relegation Fight).

***To access a free, downloadable Excel copy of the Tottenham post-relegation financial model, subscribe and email models@footyfinance.io. View only copy available here.***

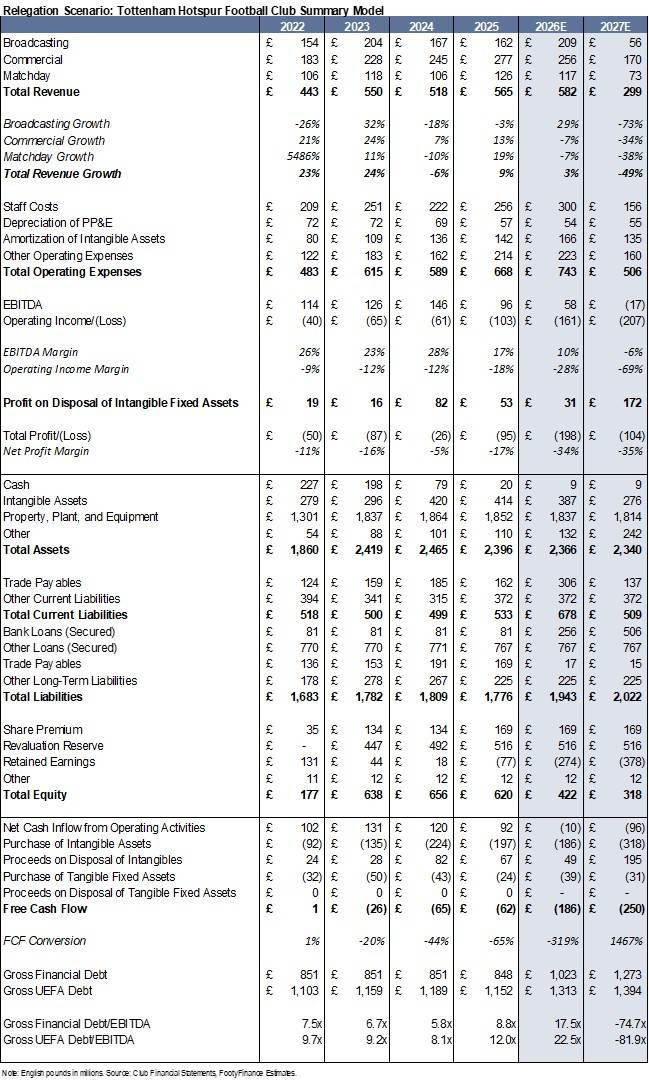

Post-Relegation Summary Financial Model

Precedent Examples – Newcastle, Aston Villa, Sunderland, Fulham, Burnley

Though no club the size of Tottenham has been relegated in the modern era, several precedent relegation examples in the last ten years including Newcastle, Aston Villa, Sunderland, Fulham, and Burnley provide insight into the financial impact of a drop to the second.

Revenue

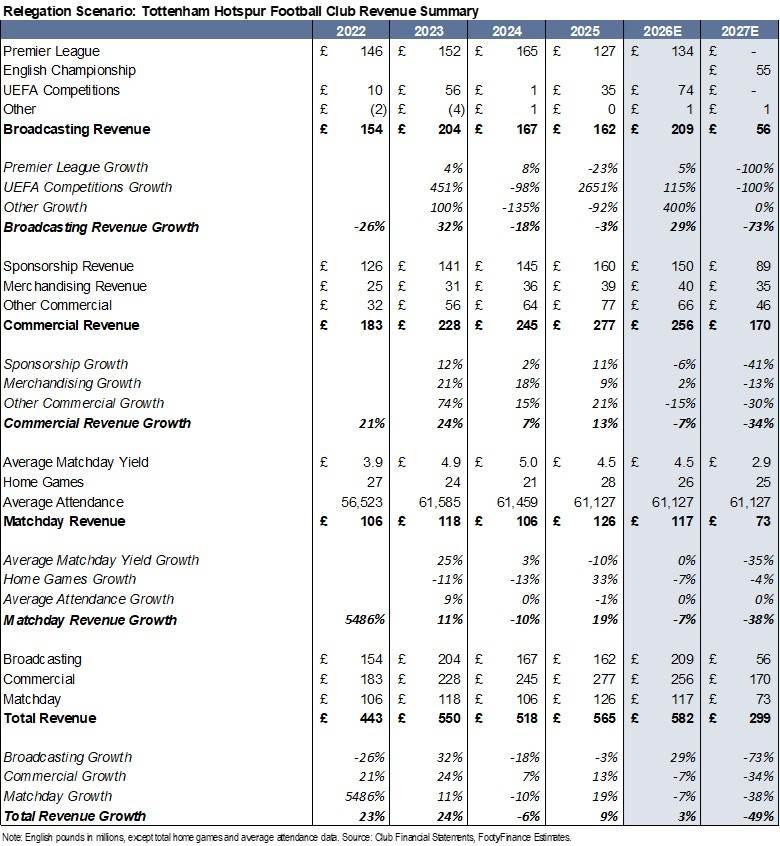

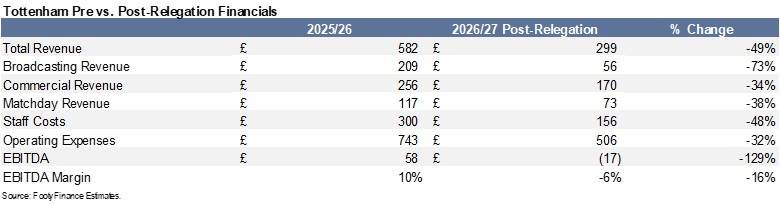

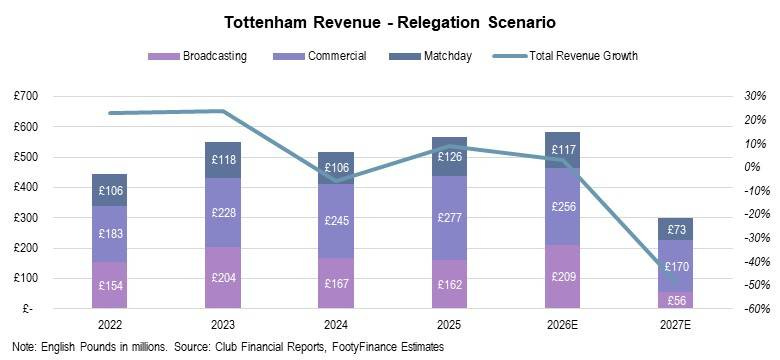

Overall, total Revenue is expected to drop 49% to £299mm in the first season in the Championship vs. £582mm expected in the 2025/26 season.

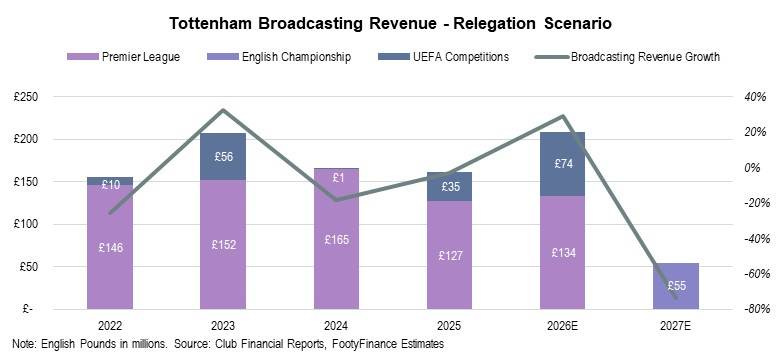

Broadcasting Revenue

Broadcasting is the greatest contributor to total revenue decline (-73% y/y). Parachute payments in the 2024/25 season (most recent season with published financials) for first year relegated clubs were ~£50mm (link). These clubs also received ~£5mm as a “basic award.” Tottenham is assumed to receive Broadcasting revenue in-line with historical precedent for first year Championship clubs (~£55mm).

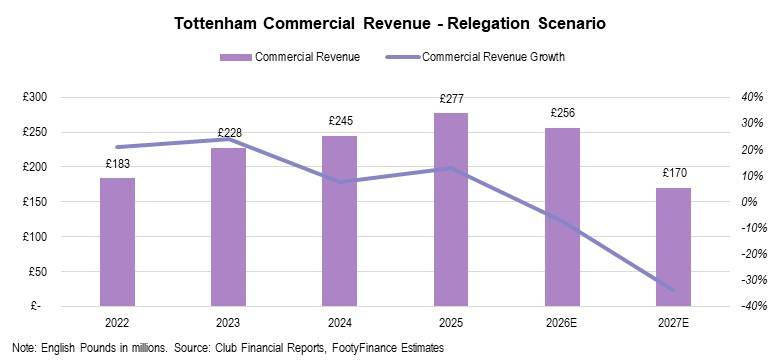

Commercial Revenue

Commercial revenue is forecasted to decline 34% post-relegation to £170mm (vs. £256mm expected in the 2025/26 season). Per press reports, Tottenham are already facing a Commercial revenue hit of “tens of millions” (even without relegation) following subpar EPL performance this season. If relegated, Tottenham likely faces further renegotiation/opt-outs of current sponsorship deals.

Nike Kit Deal: Tottenham currently earns £30mm per year from the club’s kit manufacturing agreement with Nike. The deal runs through the end of 2032-33 season as part of a long-term agreement originally signed in 2017 (link). Tottenham also retains merchandising rights in-house as part of the deal. As a result, the contract is likely structured around a minimum annual guarantee, limiting downside volatility relative to performance-sensitive commercial streams. Accordingly, FootyFinance assumes a modest 10% decline in Nike-related revenue in a post-relegation season, reflecting some pressure on global merchandise demand but no immediate contractual reset.

Merchandising: Tottenham reported Merchandising revenue of £39mm for the 2024/25 season, with £40mm expected for the 2025/26 season. Merchandising revenue is likely to see limited immediate impact from relegation, as Tottenham retains merchandising rights in-house and benefits from a global fanbase and strong brand recognition. Prolonged absence from the Premier League would likely weigh on demand over time, particularly as on-pitch performance and global relevance decline. FootyFinance assumes merchandising revenue remains relatively resilient in the near-term, with downside risk skewed toward a gradual, multi-year absence from the Premier League.

Shirt Sponsors (AIA and Kraken): The most significant pressure on Commercial revenue is likely to come from Tottenham’s primary and secondary shirt sponsorships with AIA Group and Kraken, respectively. AIA currently pays ~£40mm per year, with Kraken contributing ~£15mm. The AIA front-of-shirt agreement runs through the end of the 2026/27 season, after which AIA transitions to a lower-value training kit partnership (link).

With just one year remaining, there is risk that AIA either renegotiates terms ahead of expiry or agrees to a materially reduced fee in a post-relegation scenario. Unlike kit manufacturing agreements, which are partially supported by global merchandising demand, shirt sponsorships are directly tied to broadcast reach and brand exposure. Absence of Premier League visibility would materially reduce the value of these partnerships.

Therefore, FootyFinance assumes a ~60% decline in front-of-shirt and secondary sponsorship revenue in a post-relegation season, reflecting either 1) renegotiated terms with existing partners, or 2) replacement agreements at materially lower values.

Other Sponsorships: Beyond AIA and Kraken, Tottenham maintains a broad portfolio of secondary commercial partnerships, including a training kit agreement with BetMGM (~£10mm per year), alongside a range of regional and category-specific sponsors captured within “Other Commercial.”

While these partnerships are also exposed to a loss of Premier League visibility, the impact is typically less severe than front-of-shirt sponsorships given their lower prominence. Training kit sponsorships, however, still carry meaningful brand exposure and are more directly tied to first-team visibility, suggesting a sharper reset in value in a relegation scenario (FootyFinance assumes a ~60% decline in training kit sponsorship revenue post-relegation). The “Other Commercial” category is expected to see 30% revenue decline given its more diversified nature across various geographies and partners.

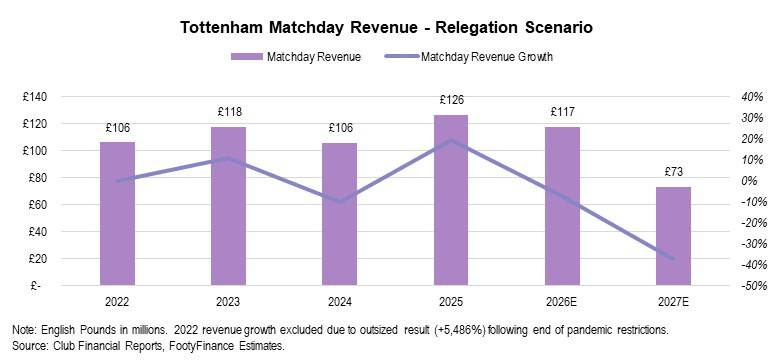

Matchday Revenue

Matchday revenue is expected to decline 38% post-relegation to £73mm (vs. £117mm expected in 2025/26), driven primarily by lower yield per fan as Championship fixtures command materially lower ticket pricing relative to Premier League and UEFA competitions. Total home match volume (25) is largely consistent with the 2025/26 season (26), as the longer Championship schedule offsets the absence of European fixtures. Attendance is assumed to remain stable at ~61,000, reflecting Tottenham’s large and loyal London fanbase. Downside risk to attendance is skewed towards a prolonged absence from the Premier League, whereas ticket pricing is expected to decline immediately following relegation.

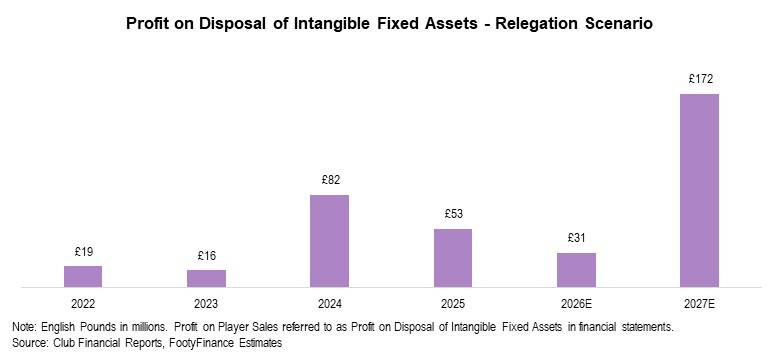

Player Sales

Player sales will be critical to maintaining financial stability post-relegation. Profit on player sales is projected at £172mm in the 2026/27 season under a relegation scenario.

Note: All player sales and purchases are assumed to occur after June 30th and thus be accounted for entirely in the 2026/27 season. Any sales and/or purchases completed prior to June 30th will be included as part of the 2025/26 financial year.

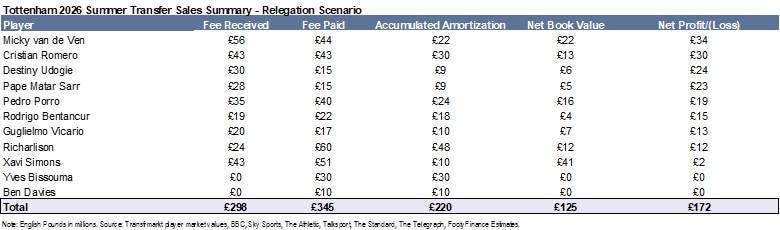

Player sale assumptions reflect a combination of expected squad turnover and financial necessity under a relegation scenario. Estimates for sale value are based on current market value via transfermarkt. Press reports consistently point to a potential “firesale” and broader squad overhaul should Tottenham drop to the Championship (link). The players assumed to be sold post-relegation are summarized in the table below based on press reported transfer plans and contract situations warranting sale. This model is meant to provide a reasonable base case for post-relegation player sales. There is upside and downside to these estimates if more or less players are sold.

- Cristian Romero, Pedro Porro, and Guglielmo Vicario are consensus picks to be sold (link)

- Reports lean towards sale of Micky van de Ven, which seems most reasonable in a relegation scenario given his status as the highest value player in the squad

- Pape Matar Sarr and Destiny Udogie are other players assumed to be sold as a result of high market value

- Richarlison is expected to be sold due to one year left remaining on his contract as of summer 2026

- Xavi Simons assumed sold due to likely push for top-flight football

- Rodrigo Bentancur assumed sold due to injury issues and likely peak value at age 28

- The contracts for Ben Davies and Yves Bissouma will expire in 2026 and these players will likely not renew

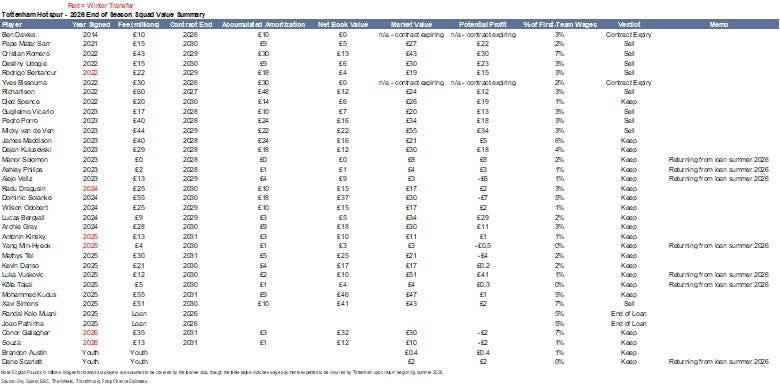

Full summer 2026 squad value summary (pre-transfer activity) for Tottenham is shown in the table below.

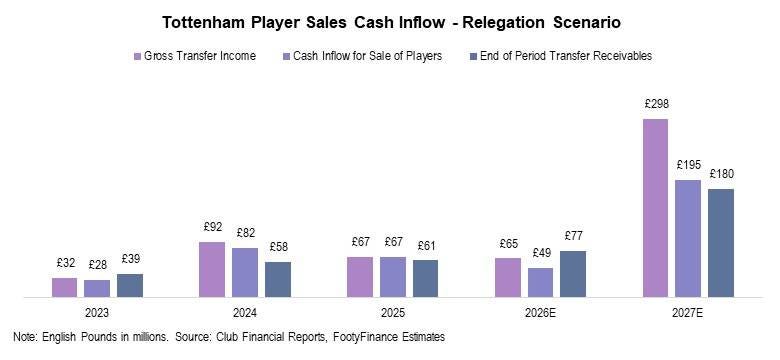

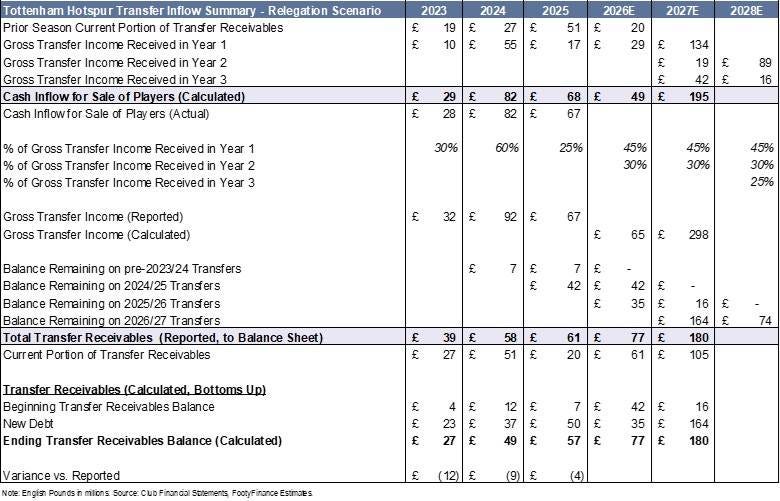

From a cash inflow perspective, Tottenham is estimated to have gross transfer income of £298mm in the summer 2026 transfer window following sales of the players mentioned above. Due to the effect of installment payments, total cash inflow from player sales is expected to be £195mm in the 2026/27 season. Full guide for methodology on forecasting player transfer-related cash flow can be found here. All forecasted summer 2026 player sales are included in the 2026/27 financial year.

To calculate cash inflow for the first forecast year (2025/26 for Tottenham), the prior season’s reported, current transfer receivables are taken and added to an estimated % of gross transfer income received (in cash) for the 2025/26 season (this % is aligned with historical trend for forecast years). To calculate gross transfer income in the forecast years, all press reported values for transfers in each season are summed together.

To calculate cash inflow for the second forecast year (2026/27), a three-year installment plan for transfer sales is assumed given there is not a current transfer receivable amount reported yet for the 2025/26 season. Year one transfer cash inflow reflects 45% of 2026/27 season gross transfer income; year two proceeds reflect 30% of 2025/26 season gross transfer income; and year three payments reflect the non-current portion of 2024/25 transfer receivables (current portion will be received in the 2025/26 season with remainder assumed to be received three seasons later in 2026/27).

The £195mm cash inflow estimate for the 2026/27 season includes £134mm related to 2026/27 transfer sales, £19mm from 2025/26 transfers, and £42mm from 2024/25 transfers.

Full transfer cash inflow summary is provided in the table below. Note that the 2028E forecasting year is used solely for calculating current transfer payable/receivable amounts for the 2027E financial year.

Player Purchases

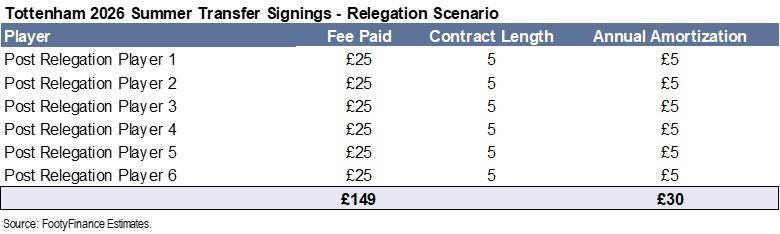

The base case model assumes that Tottenham purchases six new players post-relegation using ~half of the summer 2026 gross transfer sale proceeds. £149mm of gross transfer spend across six players yields an average purchase price of ~£25mm. All new signings are assumed to sign five-year contracts, implying annual amortization per player of £5mm (£30mm total per year).

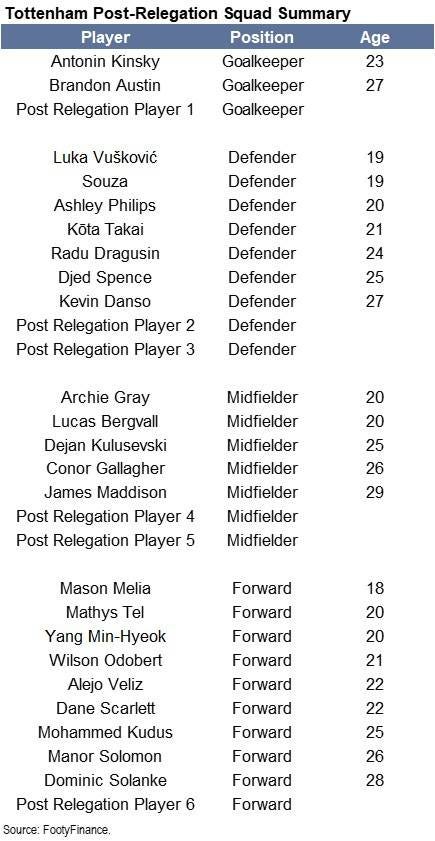

Based on expected departures, club management is likely to allocate the majority of transfer spend to defenders and midfielders. A goalkeeper will also likely be needed if Guglielmo Vicario is sold. Loan signings are also an option, but that is not the base case. EFL Championship rules stipulate that clubs are permitted to register a maximum squad of 25 senior players over age 21 for the season. An unlimited number of U-21 players are allowed. In the base case model, Tottenham will have thirteen players age 21+ entering the summer 2026 transfer window (after expected departures), leaving ample room for experienced signings. A hypothetical post-relegation squad is shown the table below.

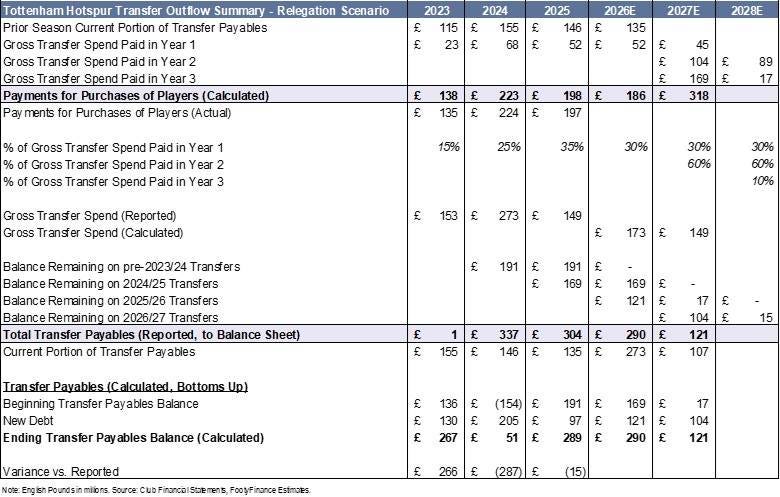

From a cash outflow perspective, Tottenham is estimated to have gross transfer spend of £149mm in the summer 2026 transfer window following the purchase of six players post-relegation. Due to the effect of installment payments, however, total cash outflow from player purchases is expected to be £318mm in the 2026/27 season as a result of high spend carrying over from prior seasons. Full guide for methodology on forecasting player transfer-related cash flow can be found here. All summer 2026 player purchases are included in the 2026/27 financial year.

To calculate cash outflow for the first forecast year (2025/26 for Tottenham), the prior season’s reported, current transfer payables are taken and added to an estimated % of gross transfer spend paid (in cash) for the 2025/26 season (for forecast years, this % is aligned with historical trend). To calculate gross transfer spend in the forecast years, all press reported values for transfers in each season are summed together.

To calculate cash outflow for the second forecast year (2026/27 for Tottenham), a three-year installment plan for transfer payments is assumed given there is not a current transfer payable amount reported yet for the 2025/26 season. Year one transfer cash payments reflect 30% of 2026/27 season gross transfer spend; year two payments reflect 60% of 2025/26 season gross transfer spend; and year three payments reflect the non-current portion of 2024/25 transfer payables (current portion will be paid in the 2025/26 season with remainder assumed to be paid ~three seasons later in 2026/27).

The £318mm cash outflow estimate for the 2026/27 season includes £45mm related to 2026/27 transfers, £104mm for 2025/26 transfers, and £169mm for 2024/25 transfers.

Full transfer cash outflow summary is provided in the table below. Note that the 2028E forecasting year is used solely for calculating current transfer payable/receivable amounts for the 2027E financial year.

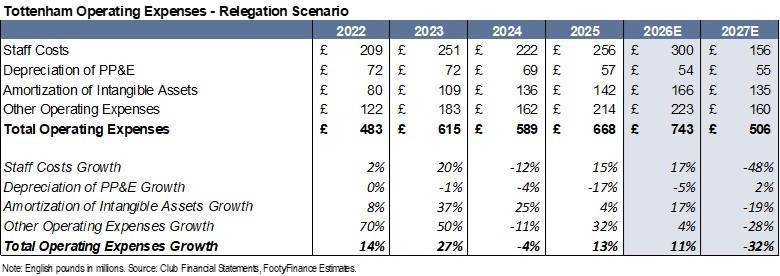

Operating Expenses

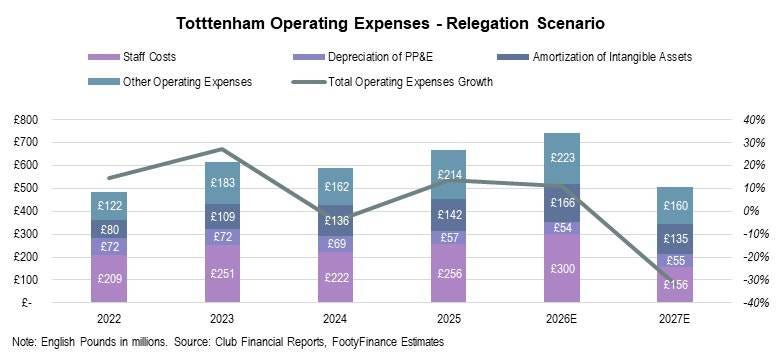

Total operating expenses are expected to decline 32% post-relegation to £506mm in the 2026/27 season. The primary driver of y/y expense decline is Staff Costs (down 48% to £156mm) – more detail below. Amortization is forecasted to see modest decline (-19% y/y). Depreciation is largely unchanged at £55mm given majority of this expense is tied to the stadium (unaffected by on-field performance).

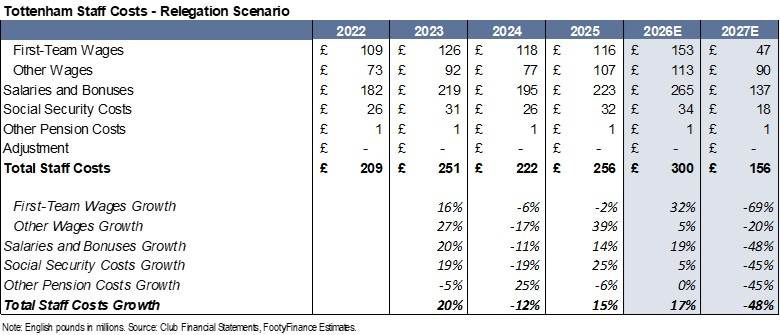

Staff Costs

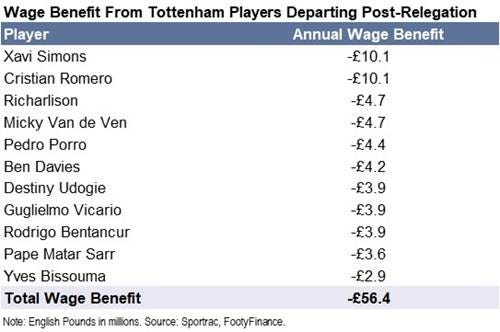

Staff Costs decline post-relegation is largely driven by the expected departure of several high wage players in addition to reported clause in Tottenham player contracts calling for mandatory salary reductions of ~50% if relegated (link). The departures of Cristian Romero, Pedro Porro, Guglielmo Vicario, Micky van de Ven, Pape Matar Sarr, Destiny Udogie, Richarlison, Xavi Simons, Rodrigo Bentancur, Ben Davies, and Yves Bissouma would be a 42% benefit to the estimated total first team wage bill of £135mm in the 2025/26 season.

In the post-relegation squad, Conor Gallagher will be the highest paid player with estimated annual wages of £5.5mm. The six post-relegation, summer 2026 signings are modeled at annual wages of £1.6mm each (£9.4mm total).

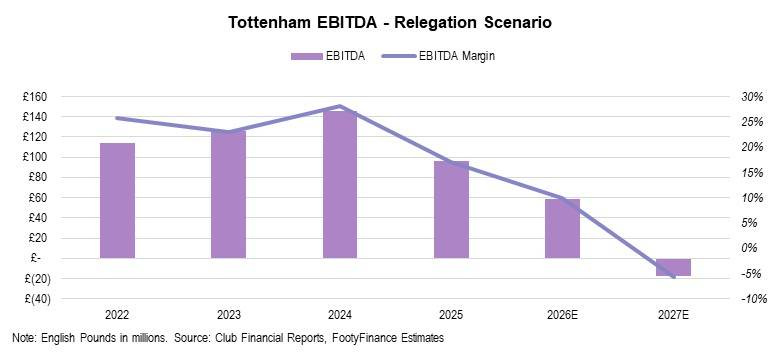

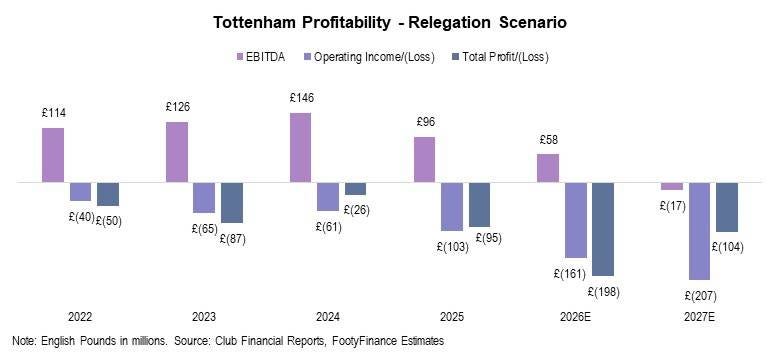

Profitability

Tottenham EBITDA is expected to decline to a -£17mm loss post-relegation (-6% margin vs. +10% margin expected in 2025/26), while Operating Loss steepens to -£207mm (vs. -£161mm expected in the 2025/26 season). Total Net Loss (-£104mm) will see a benefit from outsized profit on player sales.

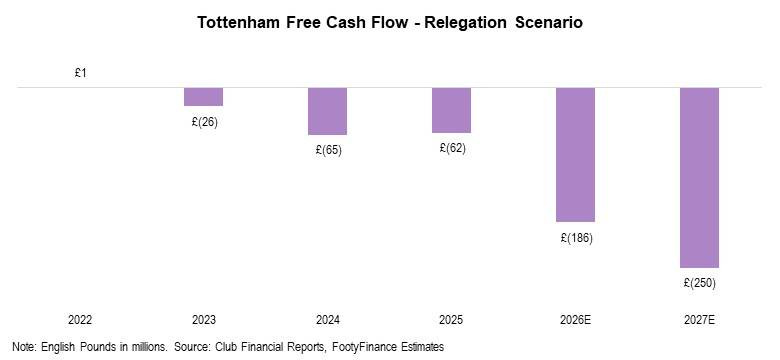

Free Cash Flow

Free Cash Flow is expected to worsen to -£250mm post-relegation (following -£186mm net outflow in 2025/26) driven by greater operating loss and increased player purchases (largely as a result of installment payments for outsized spend in recent seasons).

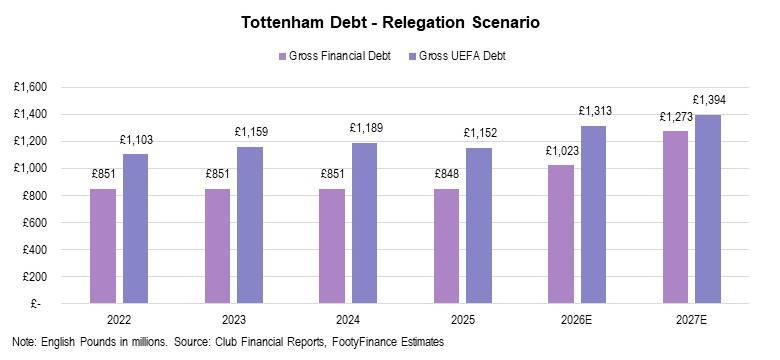

Debt

Based on expected operating trends and cash flow from player transfer activity post-relegation, Tottenham will need to raise debt and/or owner equity totaling ~£250mm in order to maintain a positive cash balance. The FootyFinance model assumes all capital raising is done through debt for the 2026/27 season. A £250mm debt raise increases gross financial debt to £1.3bn (vs. £1.0bn expected in the 2025/26 season, £848mm reported for the 2024/25 season). Gross UEFA debt (includes player transfer-related debt) rises to £1.4bn (vs. £1.3bn expected in the 2025/26 season, £1.2bn reported for the 2024/25 season).

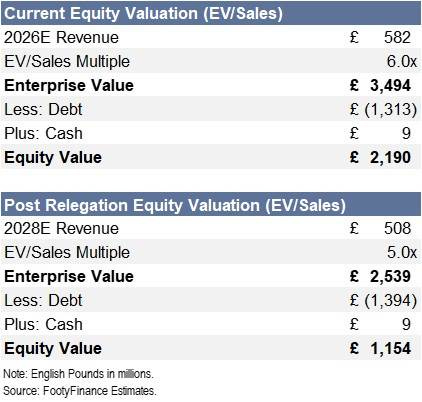

Valuation

Given Tottenham’s high likelihood to bounce back to the EPL within one season, a revenue figure similar to the 2025/26 season (minus the Champions League proceeds) should be used for valuation. Big Six clubs have been traditionally valued using an ~6x EV/Sales multiple. Relegation likely lowers the multiple closer to the 5x range. This base case scenario using 2028/29 season projected revenue of £508mm (following return to the Premier League) results in an equity valuation of £1.2bn using a 5x EV/Sales multiple (47% haircut vs. current valuation of £2.2bn based on the 2025/26 revenue forecast).

A recent example demonstrating the effect of relegation on valuation is at Leeds United following the 2022/23 season. The transaction valued Leeds at £170mm with reports indicating a valuation of £400mm had the club stayed in the Premier League for the 2023/24 season (58% decline in value).

Should Tottenham fail to bounce back within one season, then a decline in the valuation multiple is warranted. Valuation would be lower in this case given added risk of failure to be promoted back to the Premier League. However, this is not the base case.