Key Message: Tottenham is a perennial Big Six challenger with occasional runs in European competitions as most recently demonstrated by last season’s Europa League win. Per my forecast, Tottenham is on track to earn revenue of £627mm for the 2025/26 season (+12% y/y) underpinning my equity valuation of £2.7bn (based on 6.0x EV/Sales multiple). While Tottenham continues to operate with financial discipline (Big Six high EBITDA margins five out of the last six seasons), I believe the club’s current valuation is hampered by inconsistent on-field performance and high debt load. Within, I further detail initial 2025/26 financial forecast for Tottenham across all key KPIs (in addition to estimates for the not yet reported 2024/25 season). I plan to update estimates on a regular basis as the season progresses.

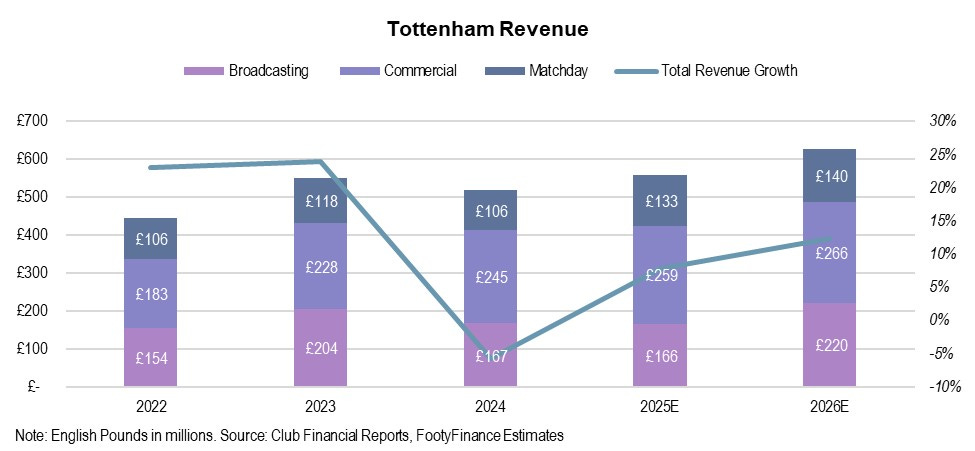

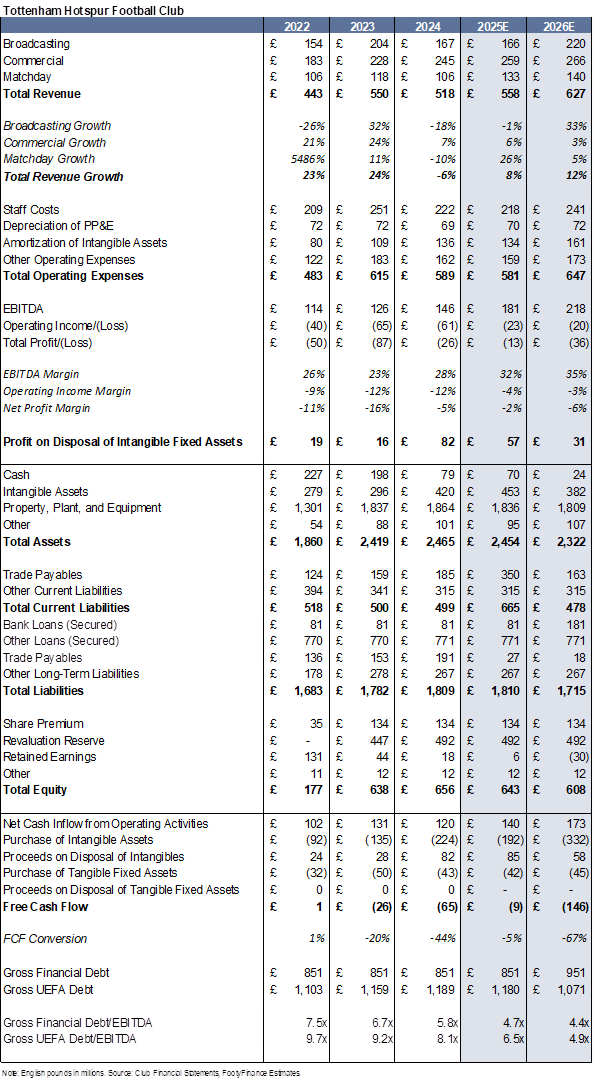

Revenue

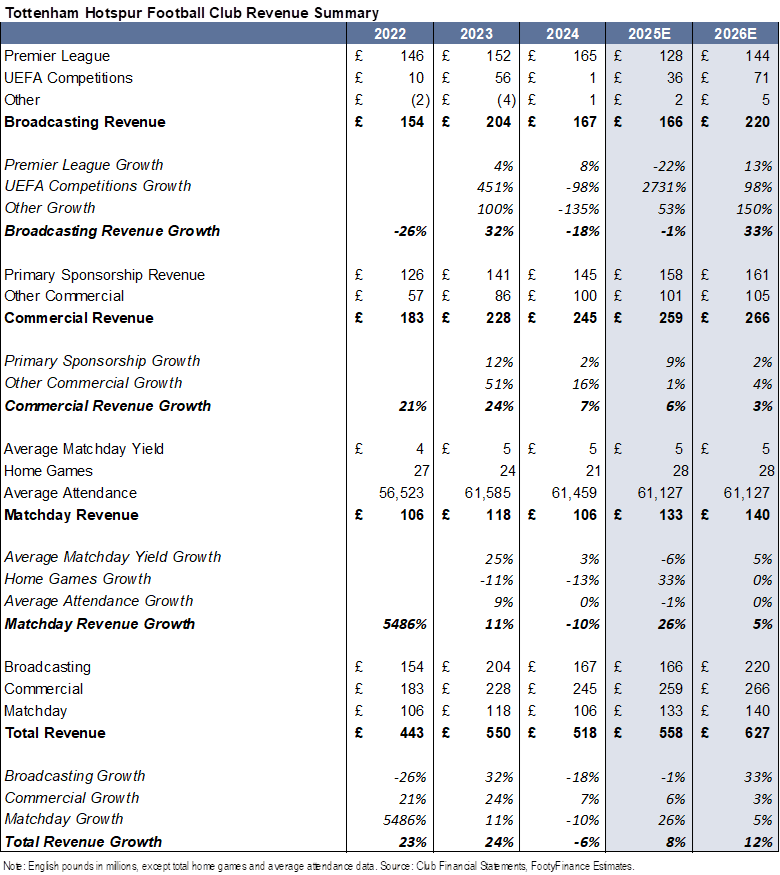

For the 2025/26 season I forecast total revenue of £627mm (+12% y/y) with gains primarily led by Broadcasting (+33%) followed by Matchday (+5%) and Commercial (+3%). I expect return of Champions League football for the first time since the 2022/23 season to drive accelerated top-line growth in the 2025/26 season.

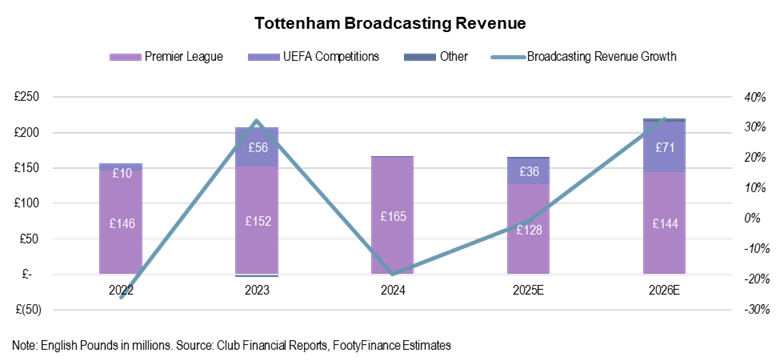

Broadcast Revenue

Based on current standing for a thirteenth place finish in the EPL, I forecast £144mm of EPL Broadcast revenue for the 2025/26 season (+13% y/y following seventeenth place finish in 2024/25 season).

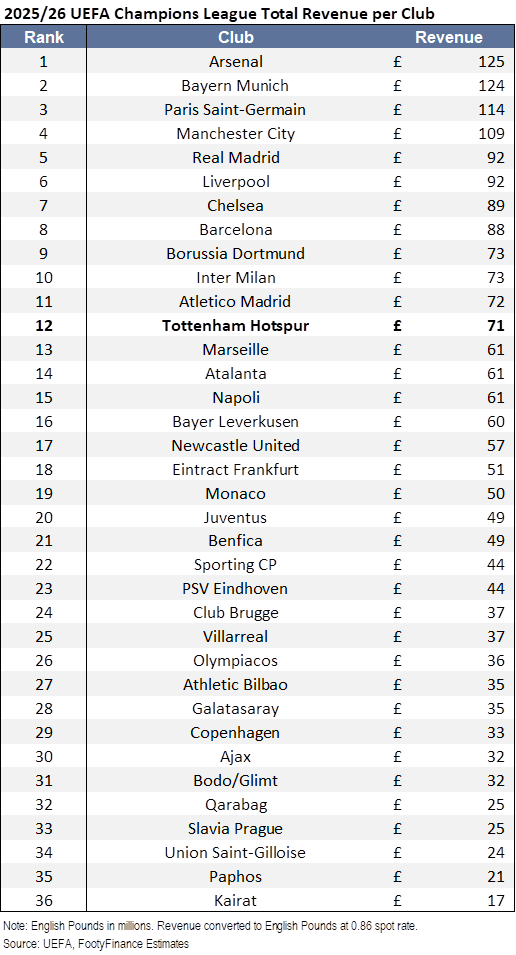

Odds for the UEFA Champions League currently value Tottenham as the twelfth most likely to win the competition. For purposes of my model pre-completion of the competition, I assume twelfth best odds to win as equivalent to reaching the Round of 16 (by way of the knockout play-offs vs. direct qualification). Exiting the Champions League in the Round of 16 garners UEFA revenue of £71mm for the 2025/26 season (+98% y/y vs. prior season Europa League winner payout).

Additionally, I model modest revenue contribution of £5mm from the EFL Cup and FA Cup.

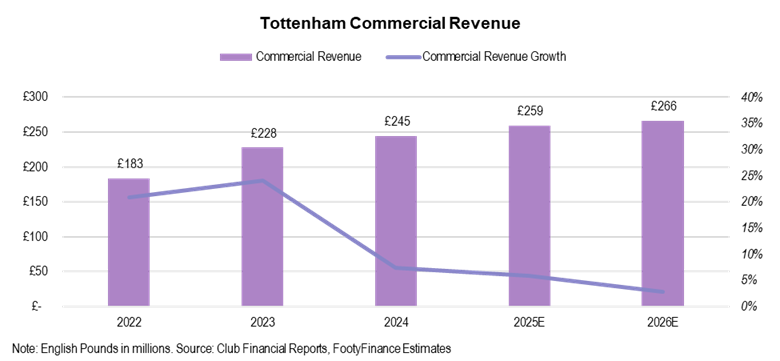

Commercial Revenue

I forecast Commercial revenue growth of +3% in the 2025/26 season (vs. +6% estimated in 2024/25). I believe primary sponsorships are consistent with prior year with minimal major changes or contract step-ups.

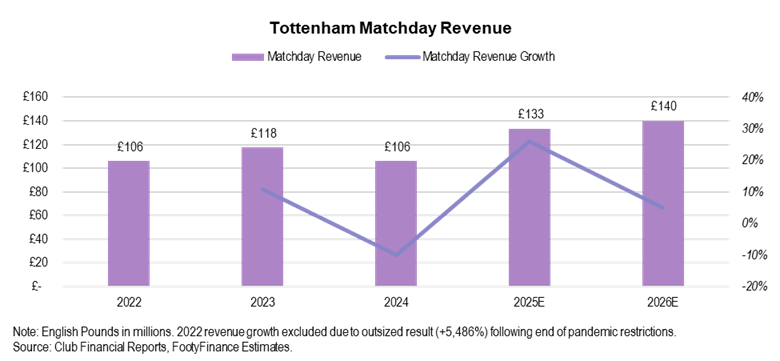

Matchday Revenue

For Matchday revenue, I expect revenue growth of +5% y/y to £140mm (vs. +26% growth in 2024/25). Strong growth in 2024/25 I believe was driven primarily by return of European football. While I expect a similar number of games in 2025/26 vs. the prior season, I believe the club will see a modest bump from return of Champions League (vs. Europa League in prior year).

Full revenue summary provided in the table below.

Player Transfers

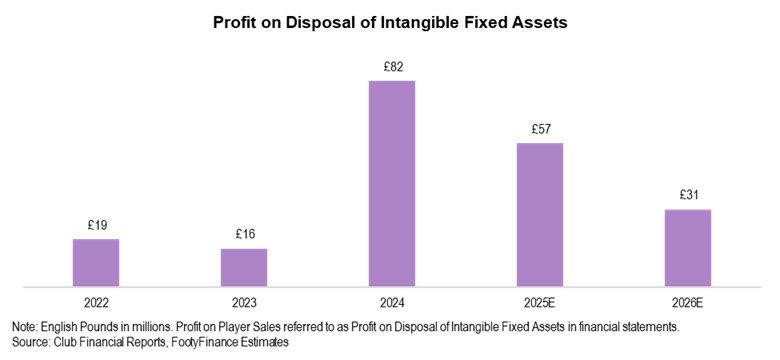

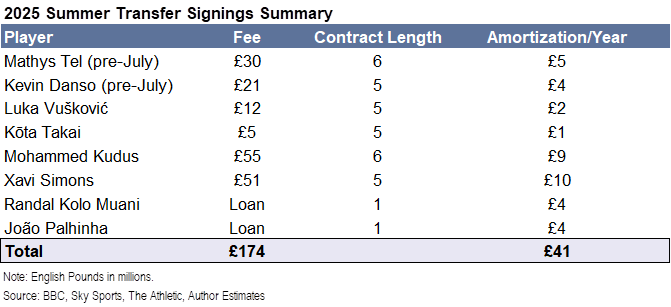

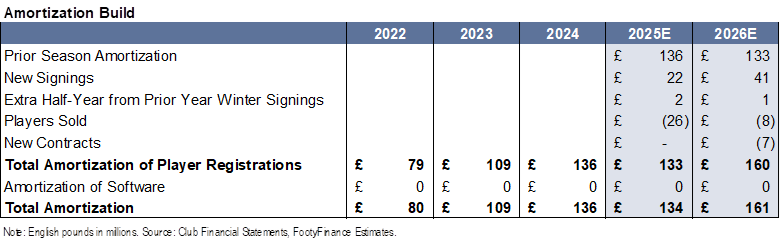

I forecast continued contribution from player sales in the 2025/26 season, though at a slightly lower level relative to recent seasons. I currently model profit on disposal of player registrations of £31mm in 2025/26 (vs. estimated £57mm profit for 2024/25 season and £39mm average from 2021/22 through 2023/24). Note that in addition to all summer 2025 transfers, 2025/26 season estimates only include completed winter 2026 transfers (Brennan Johnson in the case of Tottenham). Son Heung-Min (£19mm) was the biggest contributor to profit, per my estimates.

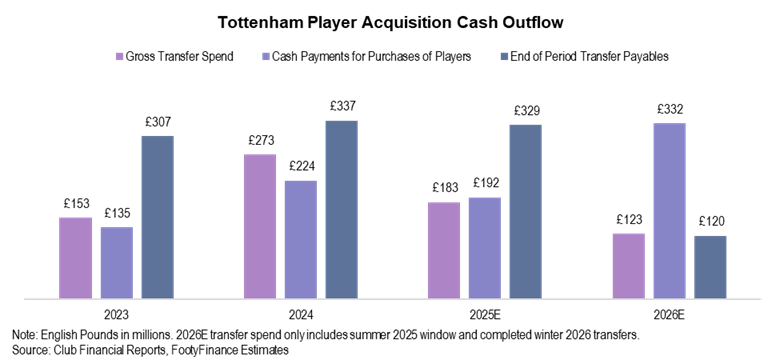

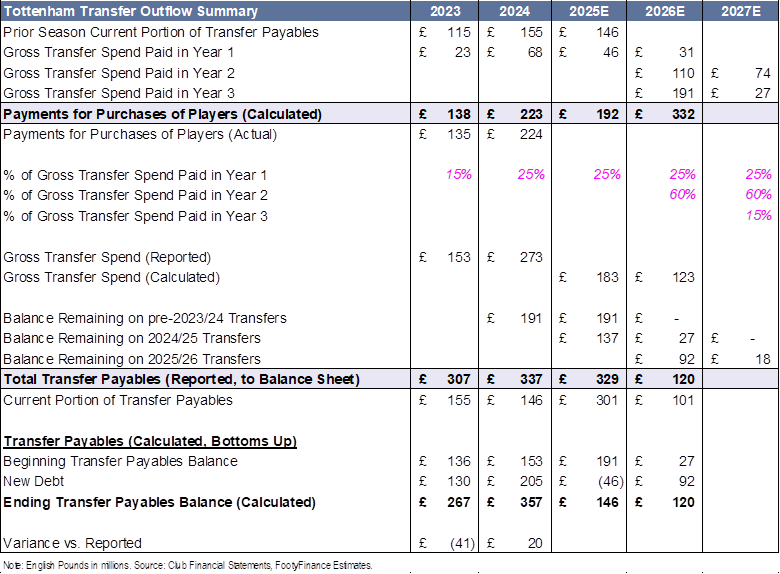

From a cash outflow perspective, I estimate gross transfer spend of £174mm in the 2025 summer window with cash outflow of £332mm for the 2025/26 season. Note that because Tottenham has a financial year end of June 30, any signings or sales made prior to July are included in the 2024/25 season results. Therefore, of this £174mm gross transfer spend, I estimate £123mm will be included in the 2025/26 financial year with the remainder in 2024/25. Summer 2025 signings included in the 2024/25 financial year are distinguished by “Pre-July” in the table below.

Because cash payments/receipts for player purchases/sales are typically paid/received through installment plans over multiple seasons, cash outflow/inflow amounts differ from gross transfer spend/income each season.

To calculate cash outflow for the first forecast year (2024/25 in the case of Tottenham), I take the prior season’s reported, current transfer payables and add that amount to an estimated % of gross transfer spend paid (in cash) for the 2024/25 season (I align this % with historical trend for forecast years). To calculate gross transfer spend in the forecast years, I sum up all press reported values for transfers in each season.

To calculate cash outflow for the second forecast year (2025/26 in the case of Tottenham), I assume a three-year installment plan for transfer payments given there is not a current transfer payable amount reported yet for the 2024/25 season. Year one transfer cash payments reflect 25% of 2025/26 season gross transfer spend; year two payments reflect 60% of 2024/25 season gross transfer spend; and year three payments reflect the non-current portion of 2023/24 transfer payables (current portion will be paid in the 2024/25 season with remainder assumed to be paid ~three seasons later in 2025/26). A full guide to my transfer cash flow and debt forecasting can be found here.

The £332mm cash outflow estimate for the 2025/26 season includes £31mm related to 2025/26 transfer sales, £110mm from 2024/25 transfers, and £191mm from 2023/24 transfers. Like player sale profit, I do not forecast potential winter transfer spend (only official spend) due to significant variability between periods. Tottenham has made no winter transfer signings as of publication of this report.

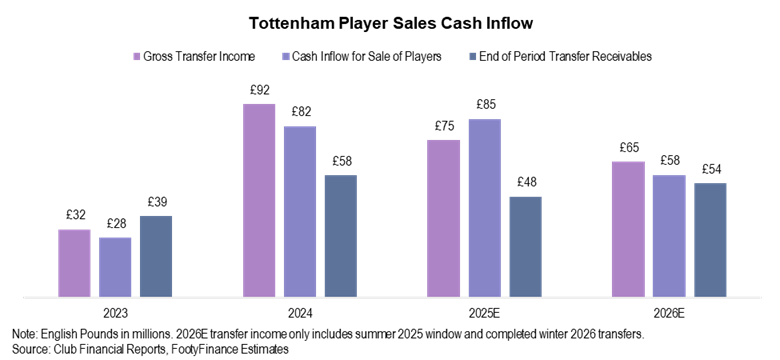

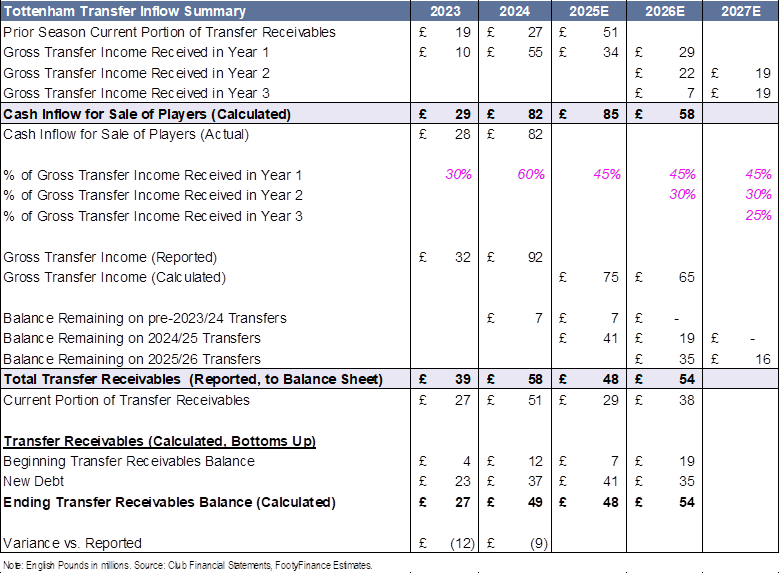

From a cash inflow perspective, I estimate gross transfer income of £65mm across the 2025 summer window and 2026 winter window with cash inflow of £58mm expected for the 2025/26 season. Forecasting for transfer cash inflow follows the same methodology as transfer cash outflows. Note that the sale of Pierre-Emile Højbjerg occurred prior to June 30 and thus is included in the 2024/25 season financial results in my model.

To calculate cash inflow for the first forecast year, I take the prior season’s reported, current transfer receivables and add that amount to an estimated % of gross transfer income received (in cash) for the 2024/25 season (I align this % with historical trend for forecast years). To calculate gross transfer income in the forecast years, I sum up all press reported values for transfers in each season.

To calculate cash inflow for the second forecast year, I assume a three-year installment plan for transfer sales given there is not a current transfer receivable amount reported yet for the 2024/25 season. Year one transfer cash inflow reflects 45% of 2025/26 season gross transfer income; year two proceeds reflect 30% of 2024/25 season gross transfer income; and year three payments reflect the non-current portion of 2023/24 transfer receivables (current portion will be received in the 2024/25 season with remainder assumed to be received ~three seasons later in 2025/26).

The £58mm cash inflow estimate for the 2025/26 season includes £29mm related to 2025/26 transfer sales, £22mm from 2024/25 transfers, and £7mm from 2023/24 transfers.

Full transfer cash outflow and inflow summary is provided in the tables below. Note that the 2027E forecasting year is used solely for calculating current transfer payable/receivable amounts for the 2026E financial year.

Expenses

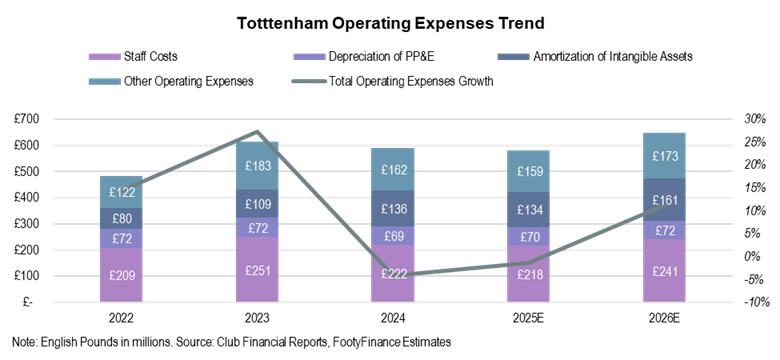

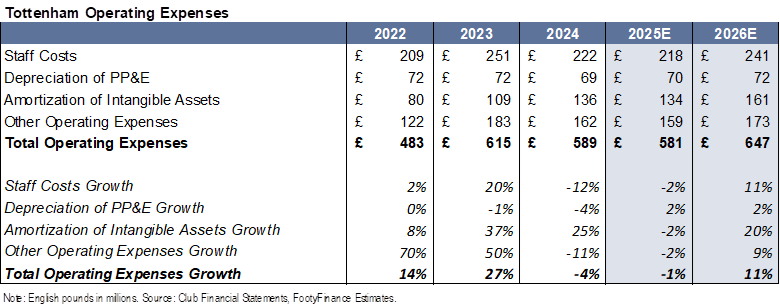

I expect Tottenham’s expense growth to accelerate in the 2025/26 season (+11% y/y) primarily driven by new player signings with Staff Costs +11% y/y and Amortization of Player Registrations +20% y/y. Note that in September, Tottenham reportedly entered into a receivables financing deal with Macquarie Group where the club raised £90mm upfront and agreed to return income from Premier League broadcasting rights for December 2025 through May 2026 as repayment (link). Based on my 2025/26 EPL revenue forecast of £144mm, and assuming ~2/3 of the revenue is subject to the Macquarie agreement (£96mm), I believe Tottenham will recognize a loss of £6mm once this debt is extinguished. I currently model this within “Other Operating Expenses.”

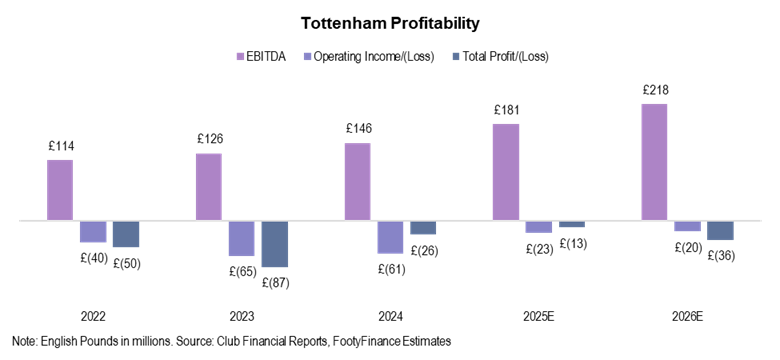

Profitability

I forecast strong EBITDA growth for Tottenham in the 2025/26 season, though expect operating income and net income to remain negative. I primarily focus on EBITDA as the key profitability metric.

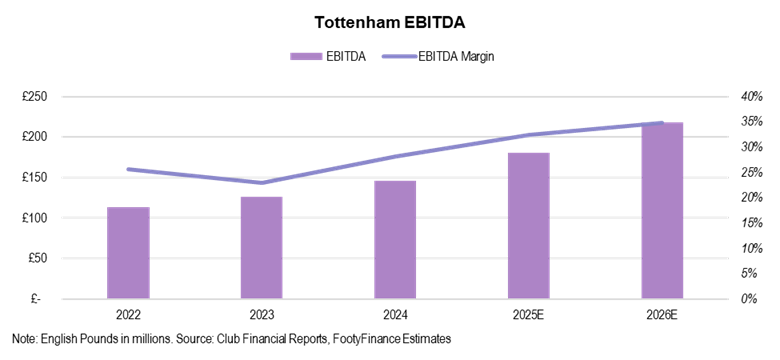

EBITDA

I expect EBITDA margin to expand in the 2025/26 season to 35% (vs. 32% estimate in 2024/25 season and 26% average for the 2021/22 through 2023/24 seasons). Per my estimates, Tottenham will see Big Six high EBITDA margin for the 2025/26 season (fifth time as Big Six leader in last six seasons).

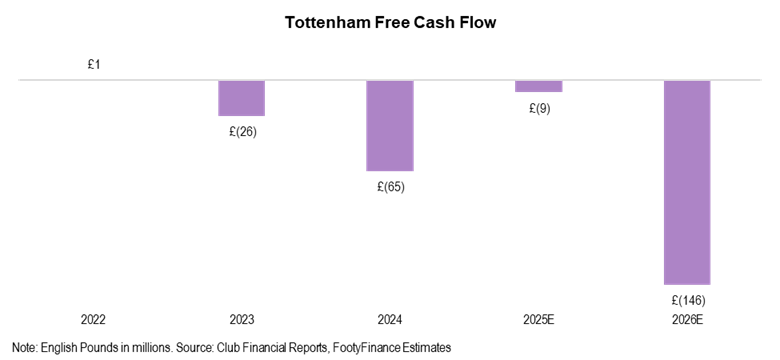

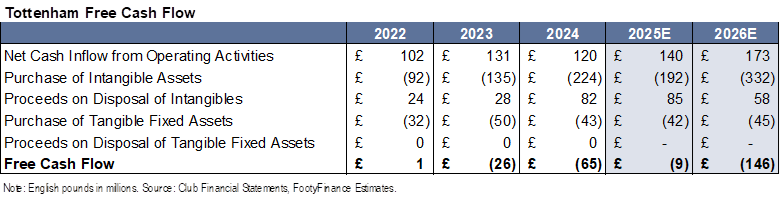

Free Cash Flow

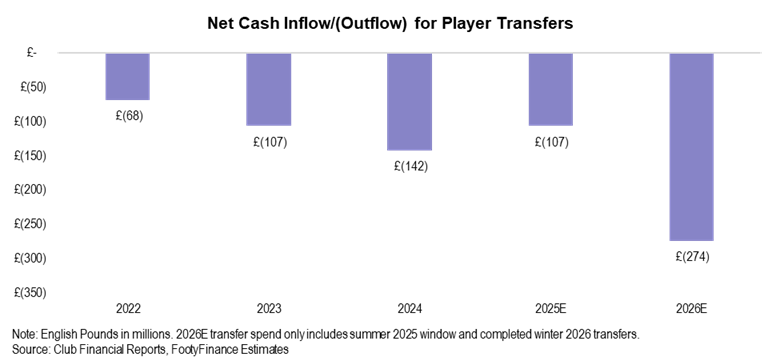

I expect Free Cash Flow (FCF) to decline in the 2025/26 season primarily driven by increased cash outflow for player purchases.

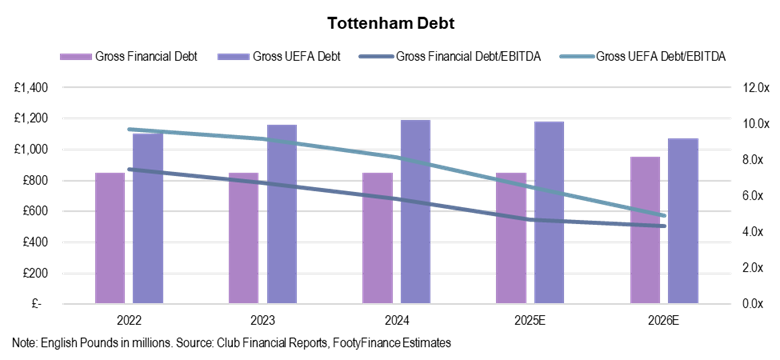

Debt

I forecast gross financial debt of £951mm in the 2025/26 season (up from most recently reported figure of £851mm in the 2023/24 season). I expect gross UEFA debt to slightly decrease from an estimated £1,180mm in the 2024/25 season to £1,071mm in 2025/26 driven by lower volume 2025 summer transfer window. My 2025/26 UEFA debt estimate is also down from most recently reported figure of £1,189mm in the 2023/24 season. On an absolute dollar basis, Tottenham has the largest debt balance amongst the Big Six which I expect is largely driven by stadium financing. Note that Financial Debt includes traditional debt instruments such as owner debt and external loans. UEFA debt adds transfer debt on top of the financial debt figure.

Valuation

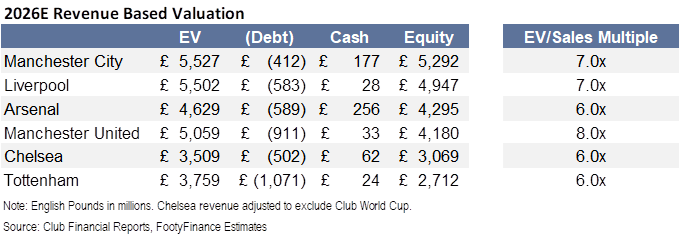

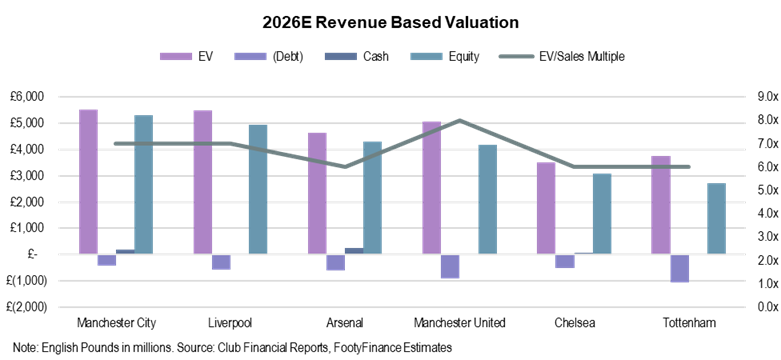

Based on my current revenue forecast of £627mm for the 2025/26 season, I value Tottenham equity at £2.7bn using a 6.0x EV/Sales multiple (in-line with ~6.0x “Big Six” average per Sportico, Forbes, and CNBC). While Tottenham is typically a top six EPL challenger with occasional runs in European competitions, I believe the club’s inconsistent on-field performance and relatively smaller commercial appeal compared to other Big Six clubs hampers the valuation multiple. Further, I believe the valuation benefit from higher matchday revenue output as a result of the new stadium is largely offset by high stadium-related debt load.

Full summary model detailed in the table below. I plan to make full excel access available at a later date.

Disclaimer

This report discusses valuation of Tottenham Hotspur Football Club for informational purposes only and does not constitute investment advice. All investment decisions should be made at one’s own risk and/or with the advice of an investment professional.

This report presents a view only as of the date of this communication and any opinions, estimates, and assumptions expressed herein are made as of the date of this communication. The information contained may be subject to change and/or withdrawal without notice or become incorrect due to passage of time and/or as a result of legal, political, economic, and other changes. FootyFinance does not assume responsibility to notify you of such changes and/or furnish an updated report. FootyFinance does not assume responsibility for results from this model.

FootyFinance is not, by making this material available, providing legal, regulatory, tax, financial, or accounting advice to the recipient of this report or any other party. Sources for the information herein are believed to be reliable, but FootyFinance makes no representation and gives no warranty as to the completeness or accuracy of the information contained herein. Past performance is not indicative of future results. No liability is accepted by FootyFinance for any losses that may arise from any use of or reliance on the information contained herein.