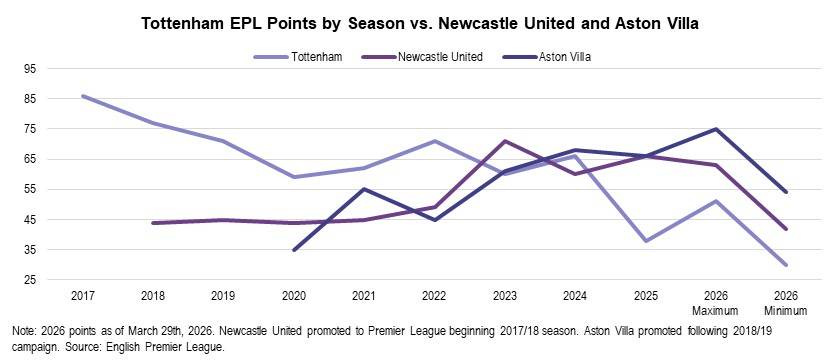

Tottenham Hotspur, a club last relegated from the English Premier League in 1977, currently sit seventeenth in the table, one point above the drop zone with seven matches to go. It is an unprecedented fall from grace for a club who reached the Champions League final just seven years ago and is universally regarded as part of England’s “Big Six.” In other words, a club so big that it’s surely impossible to get relegated?

Proof is in the Points

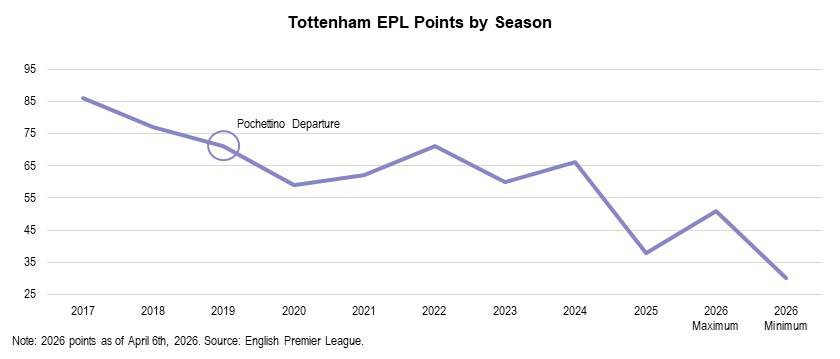

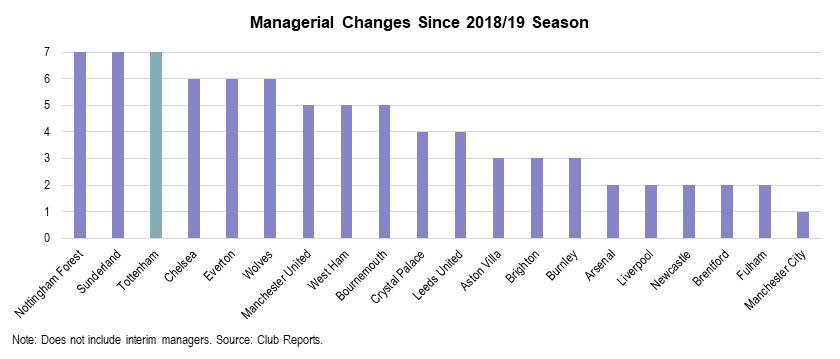

The 2018/19 season, under manager Mauricio Pochettino, was arguably the club’s peak year with a Champions League final and fourth place EPL finish. Spurs have only equaled that year’s total points tally (71) once in the seven seasons since. Key players from this era such as Harry Kane and Son Heung-min have since left, leaving Tottenham with an absence of star power. 2018/19 also marked the end of Pochettino’s tenure, with five managers across the seven seasons since 2019 causing a clear lack of tactical identity.

Overview – Drivers Behind Tottenham’s Fall

- Prioritizing Profit Creates Competitive Disadvantage

- Player Recruitment Strategy Stresses Value over Immediate Impact

- Wage Structure is Not Big Six Caliber – Resembles Big Six Chaser Pack

- High Debt Load Limits Ability to Shift Away from Cost Control Strategy

- Big Six Chaser Pack Closing Gap vs. Tottenham

- What Happens Next? – Impact of Relegation on Financial Statements and Relegation

Prioritizing Profit Creates Competitive Disadvantage

While proof of Tottenham’s decline is evident with each passing season’s points tally, the root cause can be traced back to the financial decisions of club management.

Tottenham’s fall has compounded over several years because of a strategic mismatch between financial discipline and the level of risk required to compete at the top of the Premier League. Under the leadership of Daniel Levy, Tottenham was run like a public company prioritizing margins over winning. In 2025, ahead of a fan protest, Daniel Levy said, “we cannot spend what we do not have and we will not compromise the financial stability of this club.”

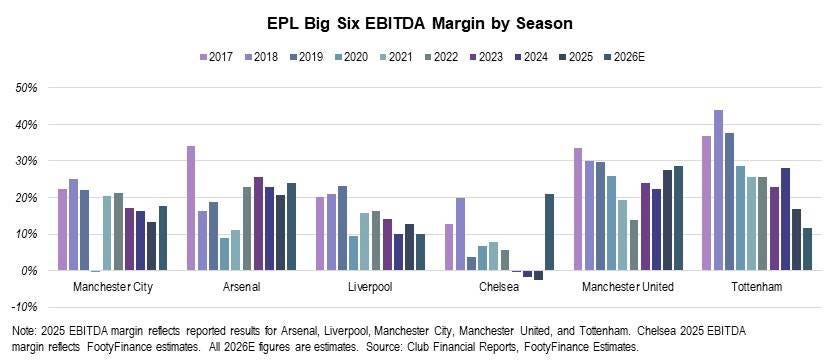

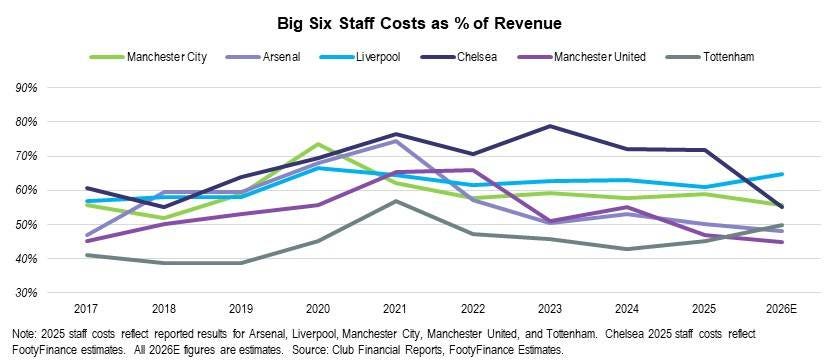

Using EBITDA as a comparable metric across the Premier League for operating profitability, Tottenham has led the Big Six in EBITDA margin for seven of the past ten seasons (2016/17 through 2025/26). Amongst all Premier League teams, Tottenham led the league in EBITDA margin for five out of eight seasons between 2016/17 and 2023/24.

If there’s one overarching reason behind Tottenham’s decline, it’s this one…to compete in the Premier League, a club must maximize points over profit.

Tottenham’s focus on maximizing profitability has led to an underinvestment in a squad needed to win. Manager churn, roster turnover, and subsequent lack of on-field identity/performance are a result of this financial decision, not a cause of it.

Disclaimer: 2024/25 and 2025/26 comparisons vs. broader Premier League are unavailable due to no forward looking financial estimates for non-Big Six clubs. EBITDA is used for profitability comparison as the metric does not count financial gain/loss from player sales and removes non-cash effects of depreciation and amortization to show pure operating performance of the club. Football clubs are in the business of winning football games, not selling players, so therefore gain/loss from player sales (which also vary significantly season to season) should be excluded when comparing operating profitability.

Player Recruitment Strategy Stresses Value over Immediate Impact

Key players from the late 2010s peak years including Harry Kane, Son Hueng-min, Christian Eriksen, and Hugo Lloris, among others, have all since left the club or retired. Who is that star player now? James Maddison? While a good player in his own right, Maddison is no Kane or Son, and more importantly, lacks a team of similar talent level around him.

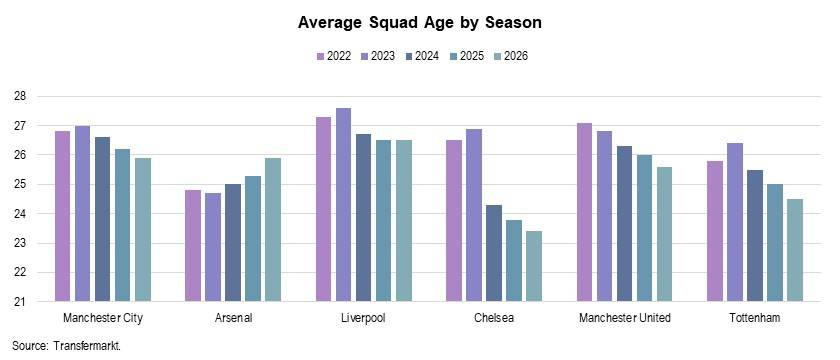

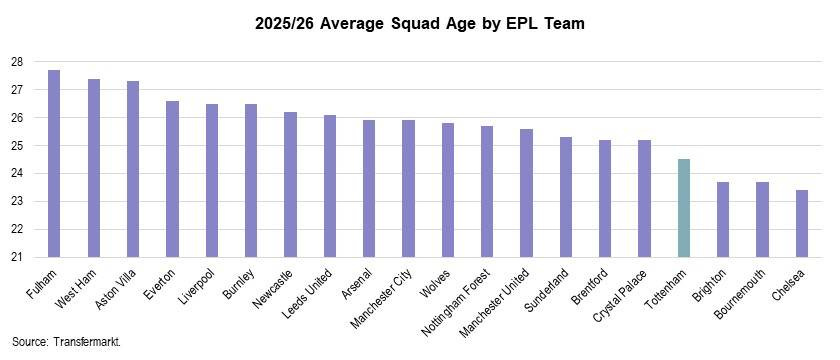

This lack of star power can be traced back to Tottenham’s player recruitment following Harry Kane’s £82mm sale to Bayern Munich in 2023 and Son’s departure in summer 2025. Spurs have emphasized value signings over immediate impact with the fourth youngest EPL squad in the 2025/26 season. Post Kane, there is a heavy skew towards under-23 recruitment with an eye toward potential —in both on-field performance and growth in a player’s financial value. No player jumps out as an immediate successor to Tottenham’s all-time record goal scorer, Harry Kane.

Tottenham have had several “almost happened” transfer signings where they ultimately lost out to another club such as Eberechi Eze in summer 2025, and Bruno Fernandes/Paulo Dybala in 2019 following the Champions League final appearance. The common denominator in these transactions is Tottenham’s reluctance to pay up in the face of competitive pressure. While wise to not overpay, Eze and Bruno Fernandes have proved to have significant, positive impact for the clubs who beat out Tottenham for their signature. Dybala is unproven in the EPL, so potential impact is less measurable.

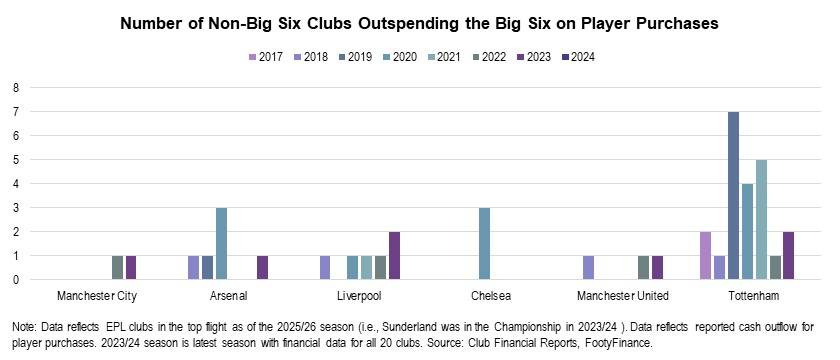

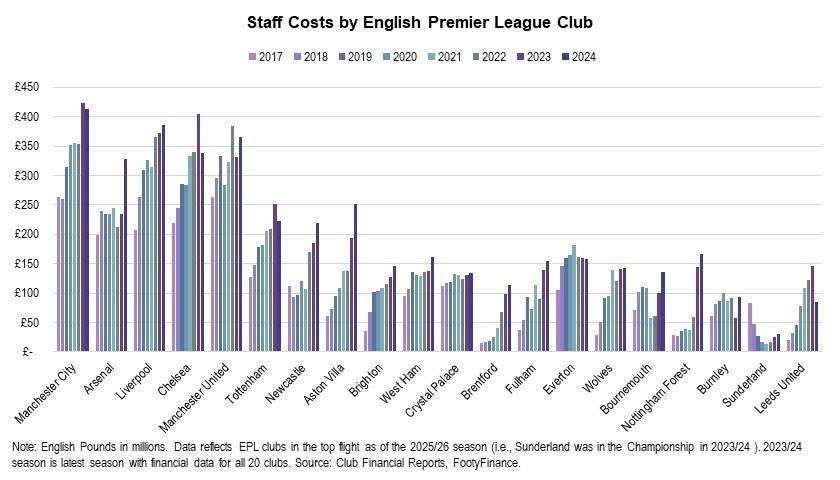

As further evidence of Tottenham’s conservative player spend, the club was outspent by at least one non-Big Six club each season between 2016/17 and 2023/24 (and as many as seven in 2018/2019). No other Big Six club was outspent each season over the same timeframe. Note that the 2023/24 season is the latest period with full financial data for all twenty Premier League clubs.

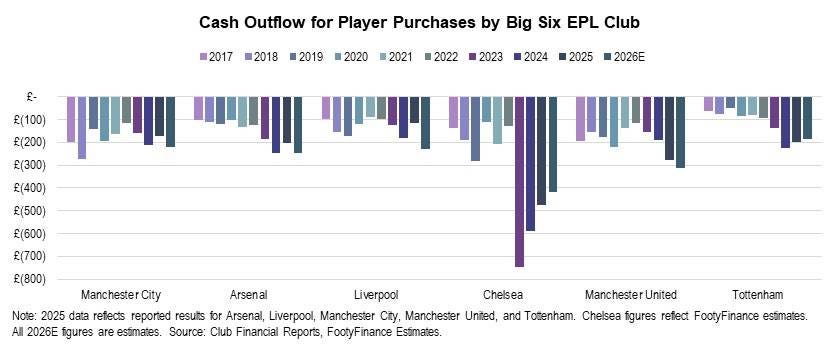

Tottenham have significantly increased transfer spend since the Harry Kane departure, though still consistently trail the rest of the Big Six. Per FootyFinance estimates, Tottenham is expected to have the lowest cash outflow for player purchases among the Big Six in the 2025/26 season. Moreover, as discussed earlier, transfer spend since Harry Kane’s departure has prioritized potential over immediate impact.

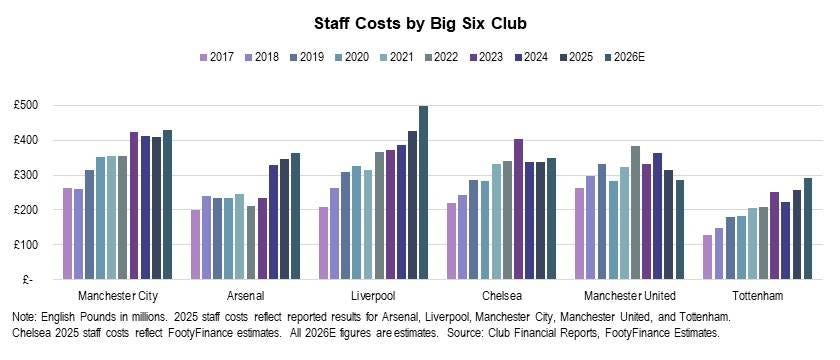

Tottenham’s Wage Structure is Not Big Six Caliber

In addition to a financially conservative player recruitment strategy, Tottenham’s wage structure for players who do actually sign lacks the caliber of other Big Six clubs.

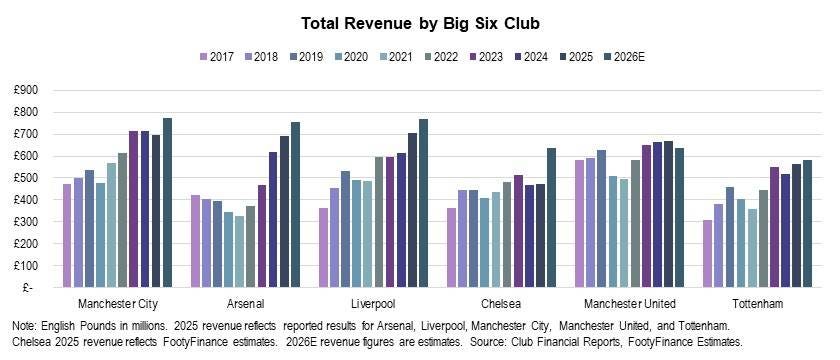

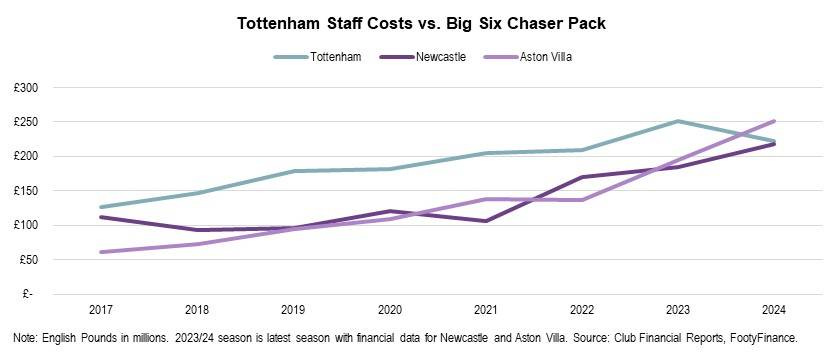

Tottenham is clearly a Big Six club in terms of revenue, but when comparing staff costs (reporting line that football clubs use for employee wages), Tottenham is more in-line with the Big Six chaser pack—Newcastle and Aston Villa.

As a % of revenue, Tottenham’s staff costs have trailed the Big Six for each of the past ten seasons. The club has Big Six caliber revenue, particularly at the commercial segment, but has failed to reinvest in the form of player salaries at a level comparable to other Big Six Clubs.

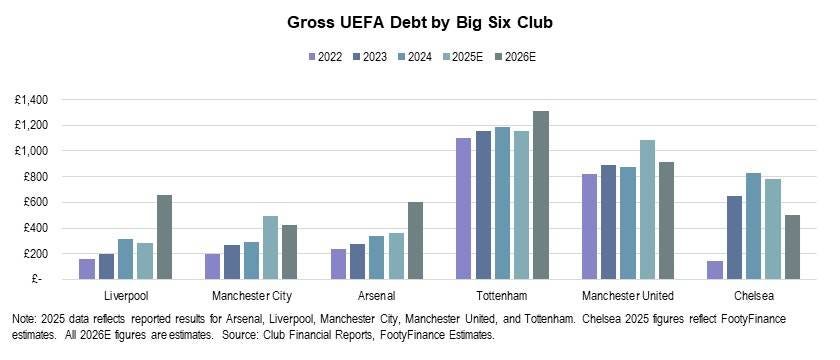

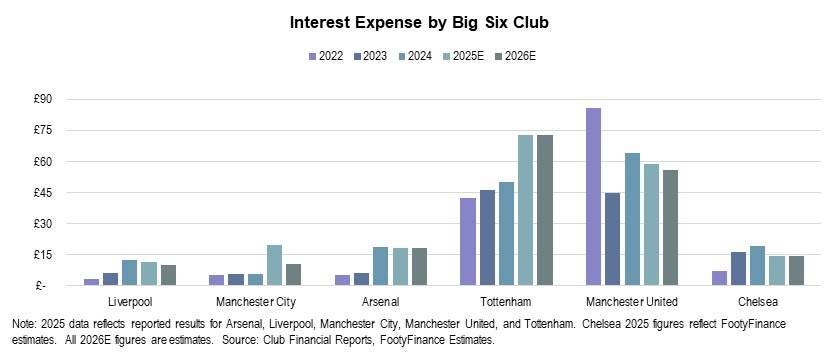

High Debt Load Limits Ability to Shift Away from Cost Control Strategy

One of the primary factors driving Tottenham’s strict cost control is the club’s ~£850mm of gross financial debt stemming from the construction of the club’s new stadium opened in 2019. Debt exceeds £1bn when factoring in player transfer-related liabilities, making Tottenham’s debt load the highest among the Big Six.

While club management may seek to distract from the high debt load by pointing out a long-dated maturity and low interest costs, an obligation to make these interest payments each year still limits spending in other areas of the club. The debt lowers valuation and hinders capital structure flexibility. It is still an obligation that cannot be written off and any CFO or potential purchaser of the club will scrutinize upwards of ~one billion pounds of debt.

Big Six Chaser Pack Closing Gap vs. Tottenham

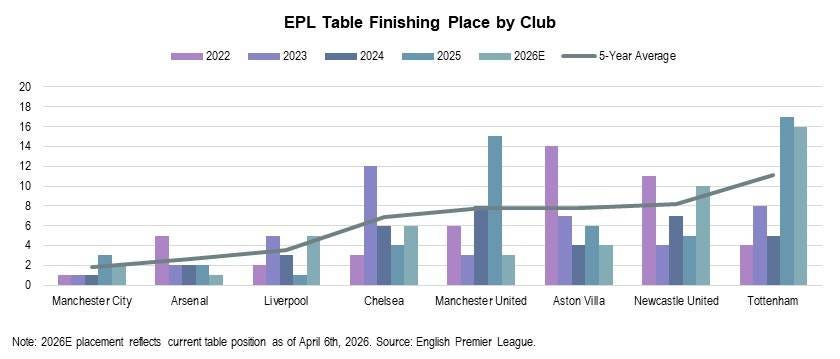

It’s already evident following a 17th place finish last season, and at best another near-relegation finish this season, but Tottenham is in serious danger of losing it’s status as a member of the Big Six. Newcastle United and Aston Villa have both outperformed Tottenham in recent seasons (top five EPL finishes and Champions League qualification) and established themselves as clear members of a Big Six chaser pack.

What’s ironic is that Newcastle United and Aston Villa were both relegated from the EPL ten years ago at the end of the 2015/16 season. Ownership has since changed with a focus on effective squad investment, and in the case of Newcastle, extra benefit from Saudi Public Investment Fund money.

What’s Next if Spurs Stay Up?

The next seven matchdays are the most important in Tottenham history. It’s do or die for a club who have not been relegated in 49 years. It’s a matter of survival, and should Spurs manage to stay up, a clear pivot in the club’s financial strategy is needed. Otherwise it’s the same story next season, and other clubs like Newcastle United and Aston Villa will inherit Tottenham’s status as a member of the Big Six.

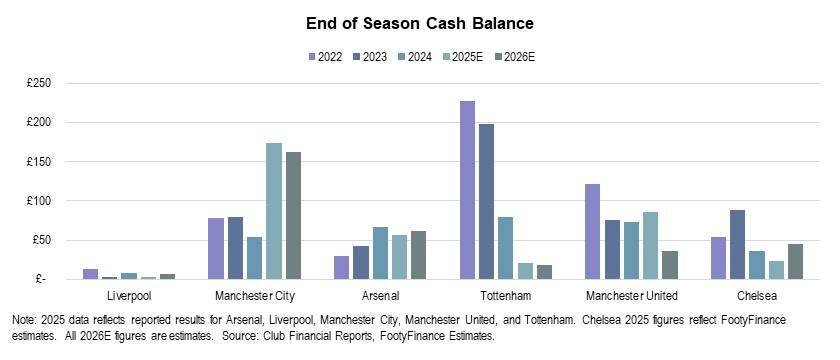

Tottenham’s cash balance at the end of the 2024/25 season was £20mm. FootyFinance models £19mm following the end of the 2025/26 season. This is the cash balance after all necessary transactions are completed by the club including player purchases, wage payments, and debt obligations. Tottenham’s highest paid player makes ~£10mm per year. Point being, there is further room for significant squad investment just using cash on hand.

Doomsday Relegation Scenario Might be a Blessing in Disguise

Should relegation occur on May 24th when Tottenham play their final match at home against Everton (or perhaps sooner), it may be a blessing in disguise. An opportunity to fully reset the club’s ethos. As mentioned earlier, both Newcastle United and Aston Villa were relegated in 2016 despite seeing significant success in the 1980’s and 90’s and being two of England’s most storied clubs. A change in ownership has driven a newfound taste of success for these two clubs.

The same can hold true for Tottenham. Relegation would likely make the club available at a significant discount to its current EPL valuation. As a longtime Big Six club, Tottenham has all the resources needed to make a quick return to the Premier League, making it an attractive proposition for potential buyers. New ownership, with a focus on adequate player investment rather than strict cost control, has the potential to spur a new era of success at Tottenham.

Sizing the Impact of Relegation on the Financial Statements and Valuation

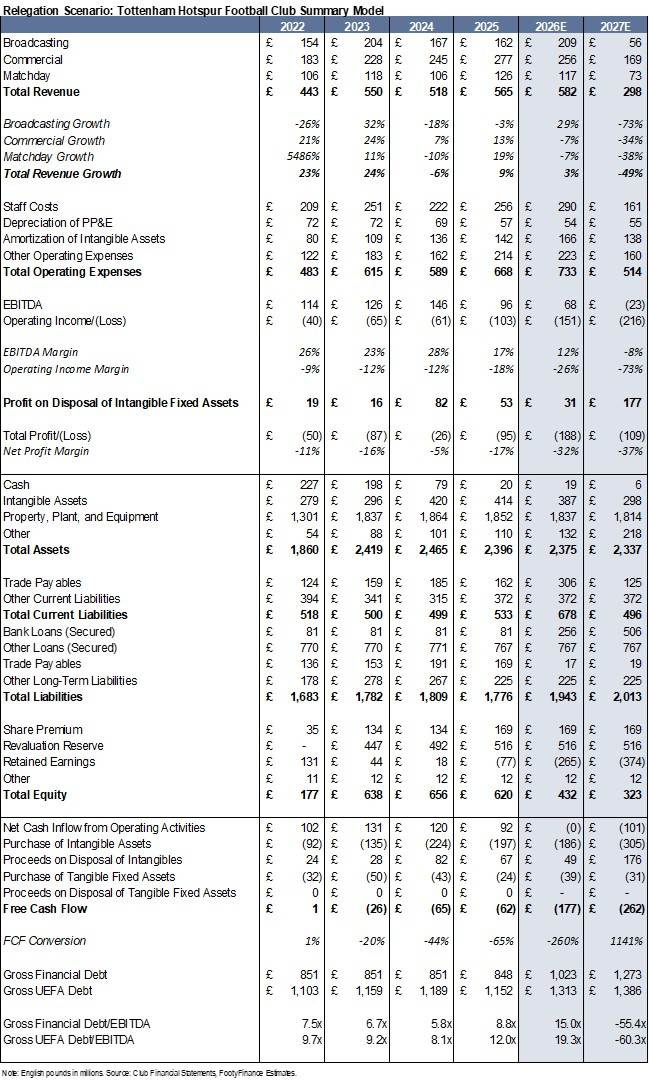

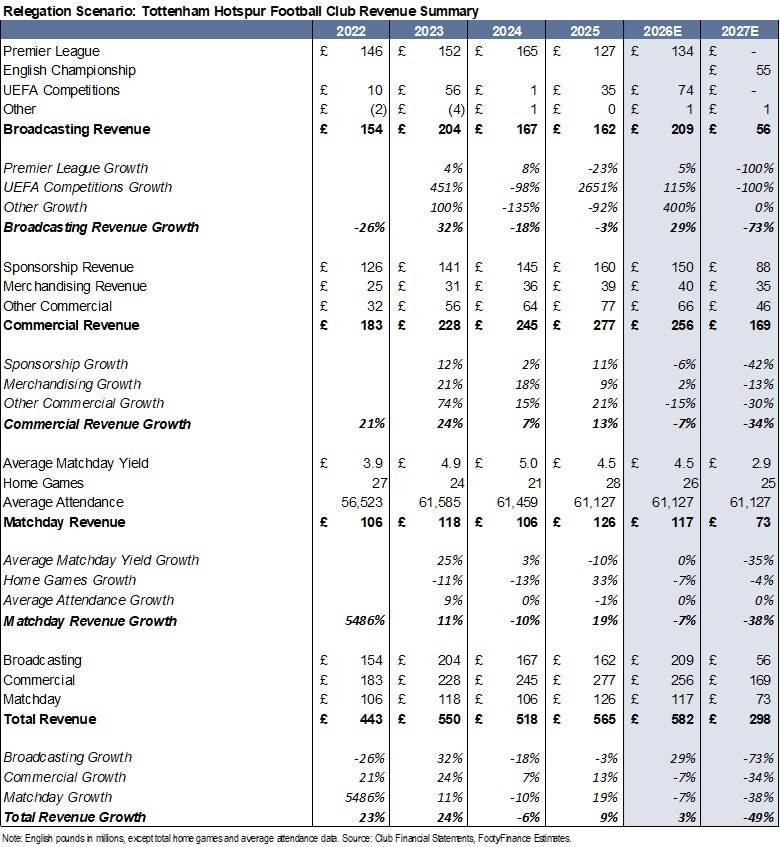

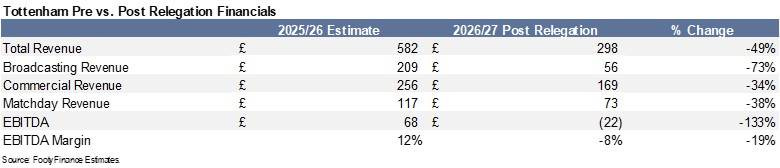

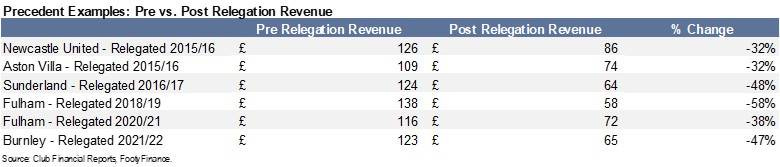

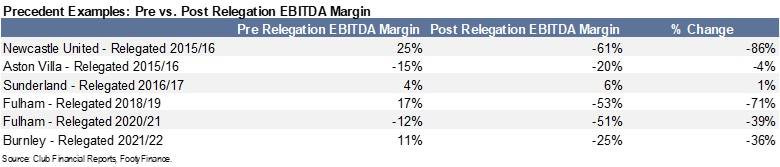

FootyFinance plans to release a separate research note analyzing Tottenham’s financial model should they drop to the Championship next season. Preliminary highlights (summary model also attached at end of this report) are total revenue of £298mm (-49% y/y) and EBITDA margin of -8% (vs. 12% projected for the 2025/26 Premier League campaign). Revenue decline is driven by projected Broadcasting segment decline of 73%, Commercial decline of 34%, and Matchday decline of 38% in the relegation scenario. Recent precedent from other clubs who have dropped in the past ten years show total revenue decline of 30-60% in the first season in the Championship. Tottenham will likely face more pressure in the Commercial segment following relegation compared to smaller clubs, which pushes estimated total revenue decline closer to 50%.

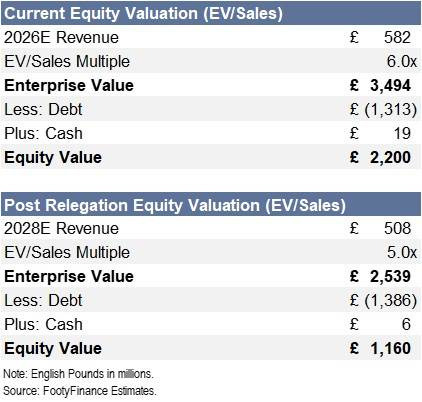

Given Tottenham’s high likelihood to bounce back to the EPL within one season, a revenue figure similar to the 2025/26 season (minus the Champions League proceeds) should be used for valuation. Big Six clubs have been traditionally valued using an ~6x EV/Sales multiple. Relegation likely lowers the multiple closer to the 5x range. This base case scenario using 2028/29 season projected revenue of £508mm (following return to the Premier League) results in an equity valuation of £1.2bn using a 5x EV/Sales multiple (47% haircut vs. current valuation of £2.2bn based on the 2025/26 revenue forecast).

A recent example demonstrating the effect of relegation on valuation is at Leeds United following the 2022/23 season. The transaction valued Leeds at £170mm with reports indicating a valuation of £400mm had the club stayed in the Premier League for the 2023/24 season (58% decline in value).

Should Tottenham fail to bounce back within one season, then a decline in the valuation multiple is warranted. Valuation would be lower in this case given added risk of failure to be promoted back to the Premier League. However, this is not the base case.

Relegation Summary Financial Model