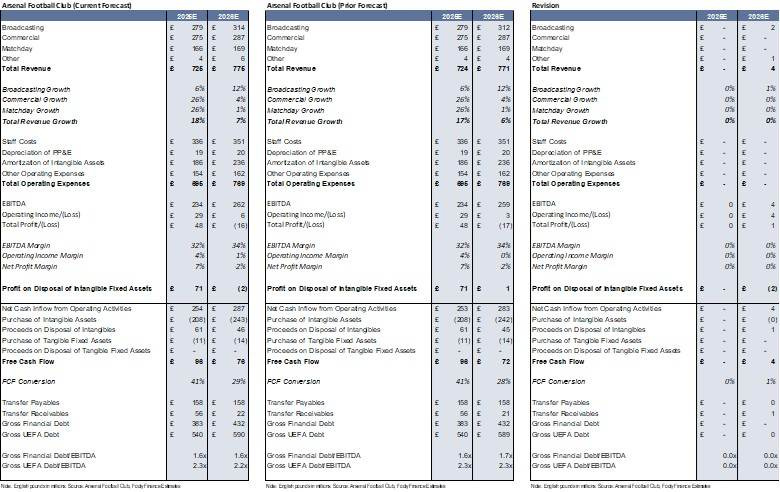

Key Message: This report details updated Arsenal model incorporating the latest Premier League/Champions League broadcasting revenue forecasts in addition to financial impacts from the January transfer window. Updates are modest with 2025/26 season total revenue estimate £4mm higher to £775mm (+7% y/y). Upward revision is driven by higher UEFA Champions League broadcasting revenue (+£2mm, latest forecast here) and slight bump in player loan income (Ethan Nwaneri to Marseille). EBITDA forecast is also £4mm higher with 100% flow through expected for the incremental £4mm revenue. True bottom line, however, is impacted by estimated -£2mm loss on sale of Oleksander Zinchenko incurred during the January transfer window. Free Cash Flow forecast is £4mm higher with increased revenue in addition to cash proceeds from Oleksandr Zinchenko sale (£1.3mm total, estimated £0.7mm received in year one, see transfer cash flow modeling guide here) more than offsetting ~£0.5mm in cash outflow for player purchases in the January window (Jaden Dixon, Evan Mooney). Arsenal is clearly the most in-form team in Europe right now with on-field success requiring minimal changes to player personnel in the January window. Overall valuation is unchanged at £4.3bn (based on a 6.0x EV/Sales multiple). Full overview of initial January 1 forecast can be found here.

Estimate Revisions

Drivers of Revisions to 2025/26 Season Forecast

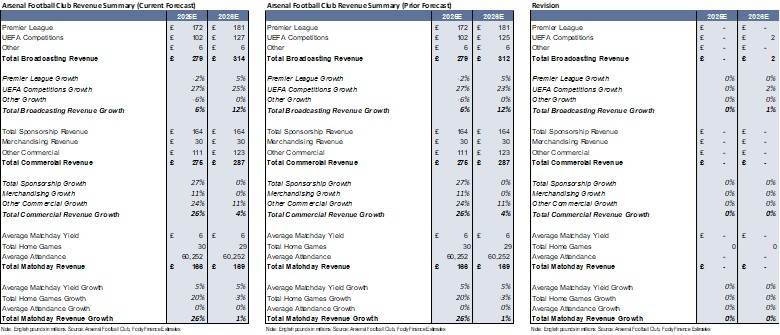

- Broadcasting Revenue: +£2mm higher based on higher UEFA Champions League revenue

- Player Trading Revenue (i.e., loan income): +£1mm higher following Ethan Nwaneri loan to Marseille

- Profit/(Loss) on Player Sales: now –£2mm loss driven by loss on sale of Oleksander Zinchenko

- Player Sales Cash Inflow:: £1mm higher from sale of Oleksander Zinchenko

- Assumed no effect to wages/operating expenses given Zinchenko was loaned to Nottingham Forest for first half of the season (wages are assumed covered by loanee club)

- Player Sales Cash Outflow: ~£0.4mm higher driven by purchases of Jaden Dixon and Evan Mooney

- Wage and amortization impact is assumed immaterial

Summary Model

Revenue

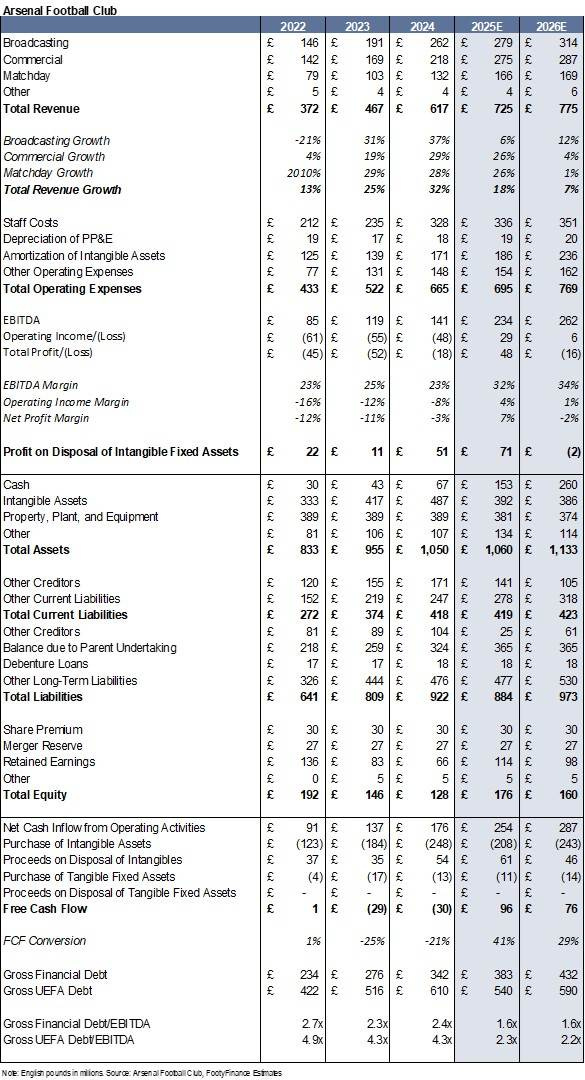

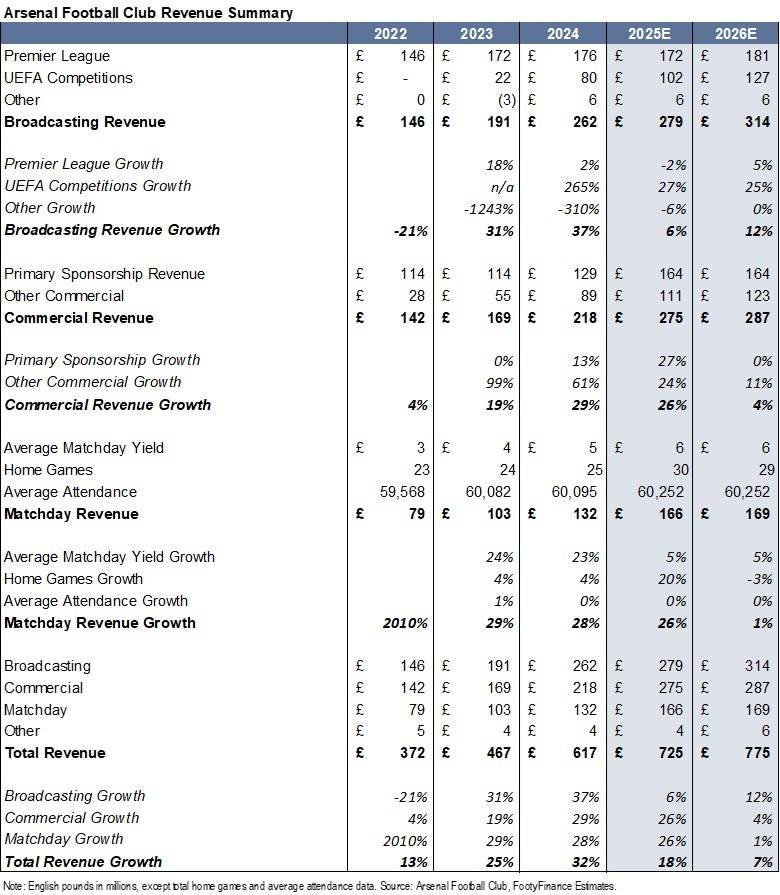

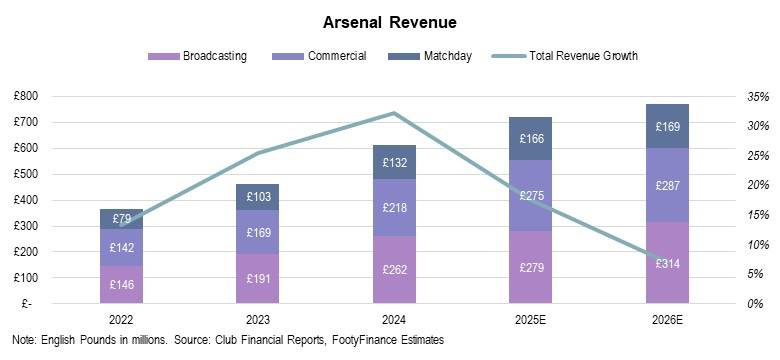

For the 2025/26 season total revenue is forecasted to be £775mm (+7% y/y) with gains primarily led by Broadcasting (+12%) followed by Commercial (+4%) and Matchday (+1%). Bottom line: sustained on field success for Arsenal continues to drive topline growth across all segments despite tough growth comparisons vs. recent seasons (+17% total revenue growth estimated for the 2024/25 season, +32% reported for the 2023/24 season).

Broadcast Revenue

Based on current standing for a first place finish, EPL Broadcast revenue is expected to come in at £181mm for the 2025/26 season (+5% y/y following second place finish in the 2024/25 season).

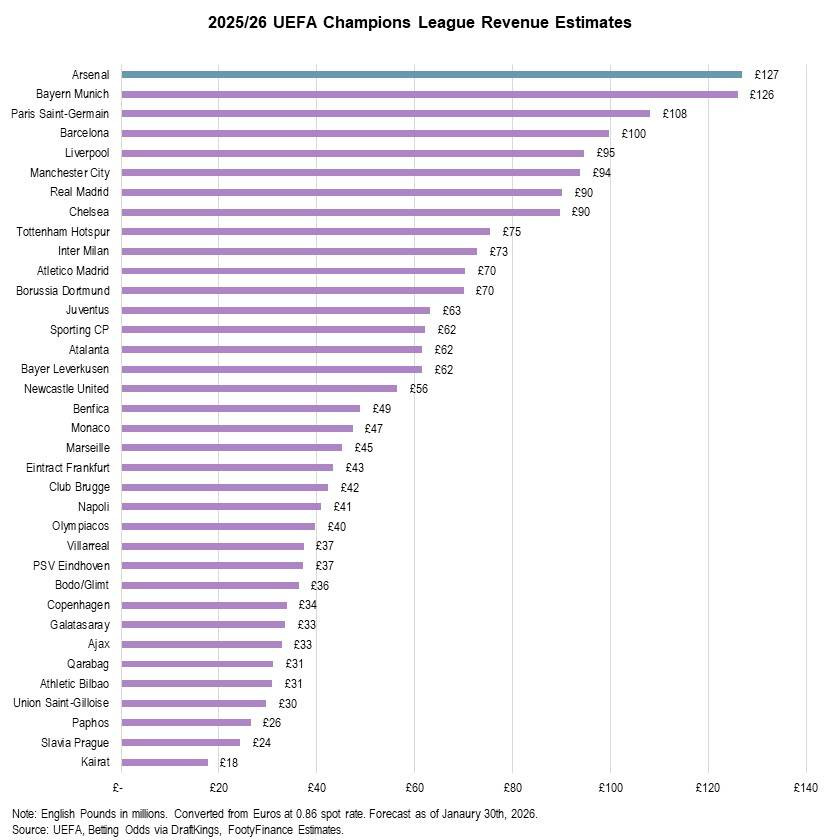

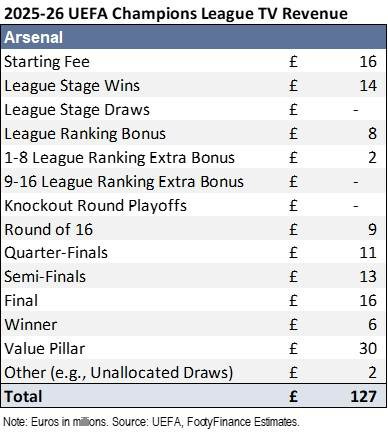

Odds for the UEFA Champions League currently value Arsenal as the most likely to win the competition. For modeling purposes pre-completion of the knockout stage, highest odds to win are assumed as equivalent to winning the competition. Winning the Champions League is expected to garner Arsenal UEFA revenue of £127mm for the 2025/26 season (+25% y/y following Champions League semi-final exit in 2024/25). See latest Champions League forecast here.

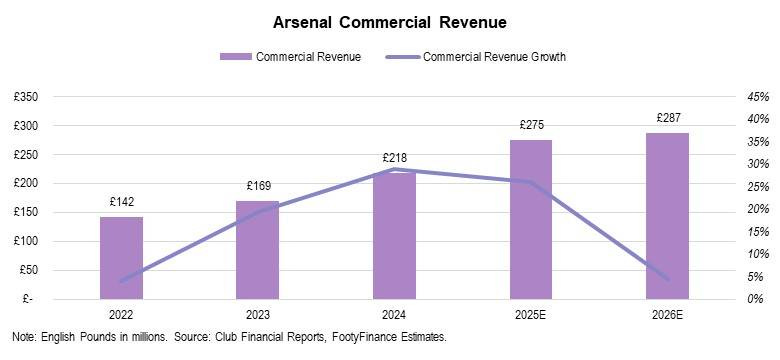

Commercial Revenue

Arsenal’s Commercial revenue growth is forecasted to decelerate to +4% in the 2025/26 season (vs. +26% estimated in 2024/25) as the club laps Emirates sponsorship renewal in the 2024/25 season.

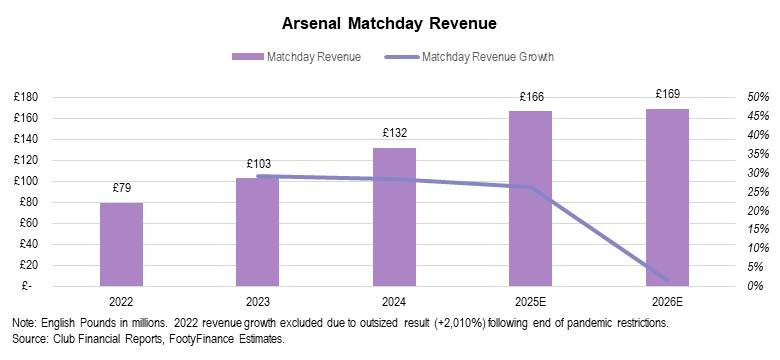

Matchday Revenue

Arsenal’s 2025/26 season Matchday revenue is expected to benefit from a deep run in the Champions League similar to the 2024/25 season. Matchday revenue of £169mm is forecasted for the 2025/26 season (+1% y/y vs. £166mm in the 2024/25 season).

Player Transfers

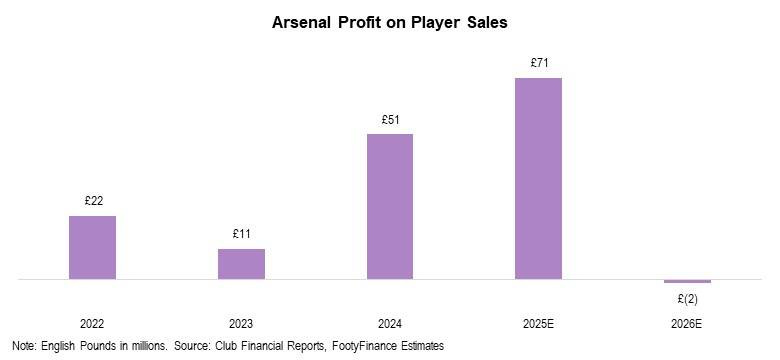

Arsenal is forecasted to see a loss on disposal of player registrations of -£2mm for the 2026/26 season driven by primarily loss on sale of Oleksandr Zinchenko in the January window, partially offset by £1mm gain on summer 2025 sales. The -£2mm loss compares to an estimated £71mm profit for the 2024/25 season and £28mm reported average from 2021/22 through 2023/24.

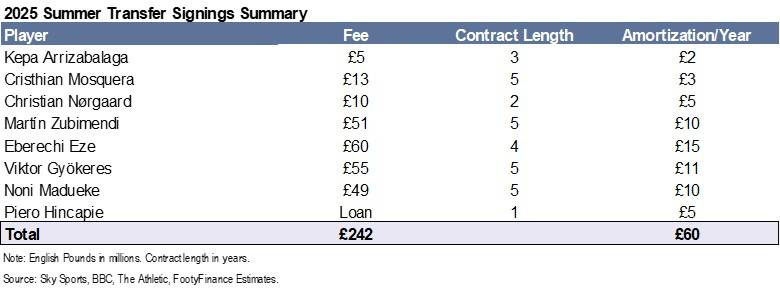

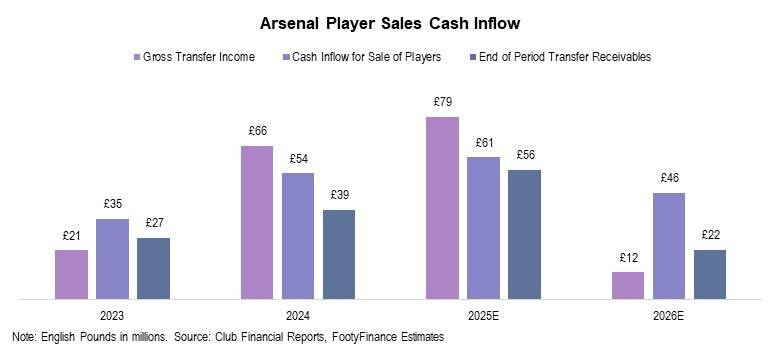

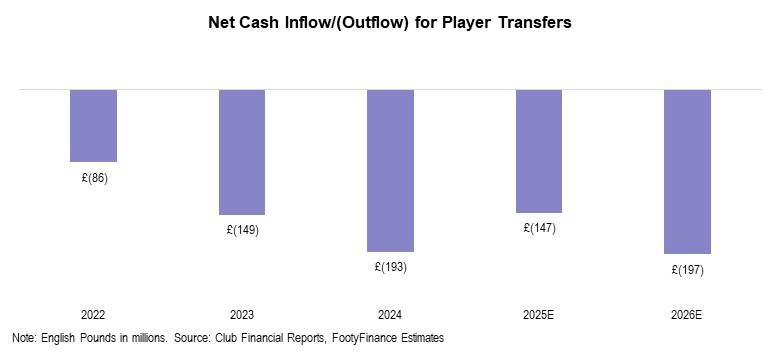

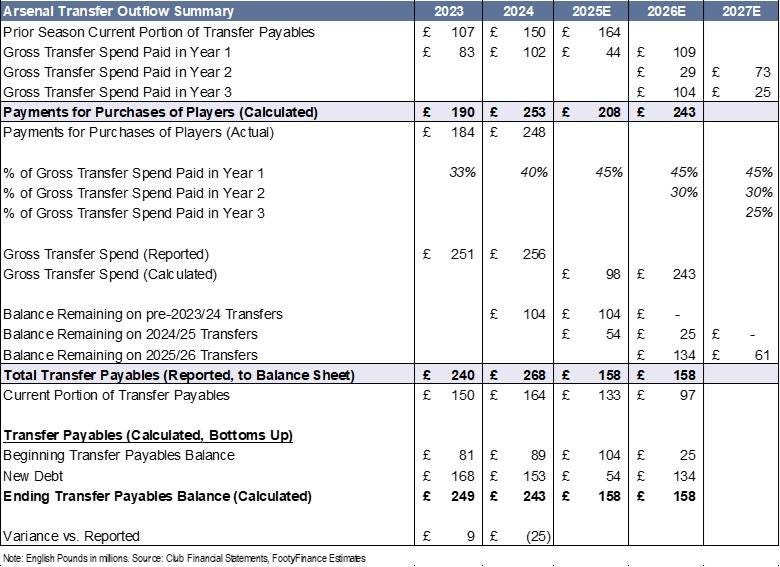

From a cash outflow perspective, Arsenal is estimated to have gross transfer spend of £242mm in the 2025 summer window and £1mm in the January 2026 window. Note that because cash payments/receipts for player purchases/sales are typically paid/received through installment plans over multiple seasons, cash outflow/inflow amounts differ from gross transfer spend/income each season. Arsenal is forecasted to have total cash outflow of £243mm for the 2025/26 season. Gross transfer spend and total cash outflow for player purchases equaling the same amount in the 2025/26 season (£243mm) is simply a coincidence.

To calculate cash outflow for the first forecast year (2024/25 in the case of Arsenal), the prior season’s reported, current transfer payables are taken and added to an estimated % of gross transfer spend paid (in cash) for the 2024/25 season (for forecast years, this % is aligned with historical trend). To calculate gross transfer spend in the forecast years, all press reported values for transfers in each season are summed together.

To calculate cash outflow for the second forecast year (2025/26 in the case of Arsenal), a three-year installment plan for transfer payments is assumed given there is not a current transfer payable amount reported yet for the 2024/25 season. Year one transfer cash payments reflect 45% of 2025/26 season gross transfer spend; year two payments reflect 30% of 2024/25 season gross transfer spend; and year three payments reflect the non-current portion of 2023/24 transfer payables (current portion will be paid in the 2024/25 season with remainder assumed to be paid ~three seasons later in 2025/26). A full guide to transfer cash flow and debt forecasting methodology can be found here.

The £243mm cash outflow estimate for the 2025/26 season includes £109mm related to 2025/26 transfers, £29mm for 2024/25 transfers, and £104mm for 2023/24 transfers.

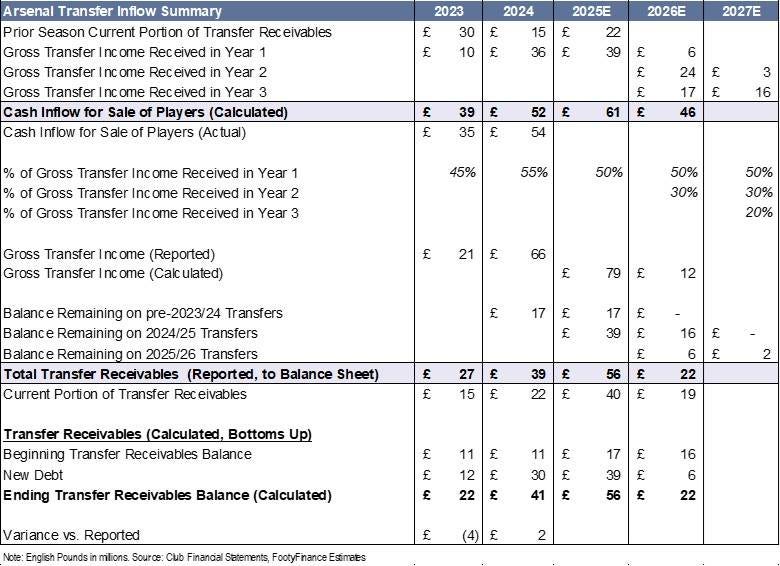

From a cash inflow perspective, Arsenal is estimated to have gross transfer income of £10mm in the 2025 summer window and £1mm in the 2026 January window. Due to effect of installment payments, total cash inflow from player sales is expected to be £46mm in the 2025/26 season. Forecasting for transfer cash inflow follows the same methodology as transfer cash outflows.

To calculate cash inflow for the first forecast year, the prior season’s reported, current transfer receivables are taken and added to an estimated % of gross transfer income received (in cash) for the 2024/25 season (this % is aligned with historical trend for forecast years). To calculate gross transfer income in the forecast years, all press reported values for transfers in each season are summed together.

To calculate cash inflow for the second forecast year, a three-year installment plan for transfer sales is assumed given there is not a current transfer receivable amount reported yet for the 2024/25 season. Year one transfer cash inflow reflects 50% of 2025/26 season gross transfer income; year two proceeds reflect 30% of 2024/25 season gross transfer income; and year three payments reflect the non-current portion of 2023/24 transfer receivables (current portion will be received in the 2024/25 season with remainder assumed to be received ~three seasons later in 2025/26).

The £45mm cash inflow estimate for the 2025/26 season includes £6mm related to 2025/26 transfer sales, £24mm from 2024/25 transfers, and £17mm from 2023/24 transfers.

Full transfer cash outflow and inflow summary is provided in the tables below. Note that the 2027E forecasting year is used solely for calculating current transfer payable/receivable amounts for the 2026E financial year.

Expenses

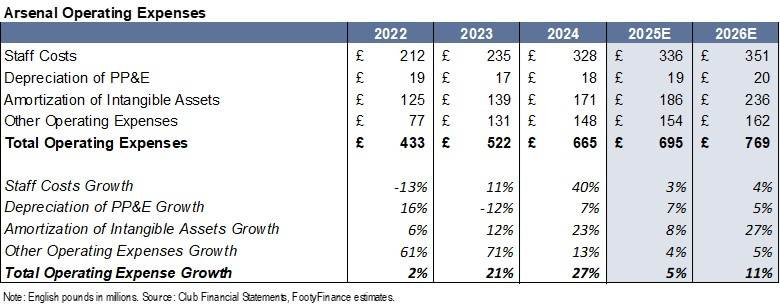

Expense growth is expected to accelerate in the 2025/26 season (+11% vs. estimated +5% in the 2024/25 season) primarily driven by new player signings with Staff Costs +4% y/y and Amortization of Registrations +27% y/y.

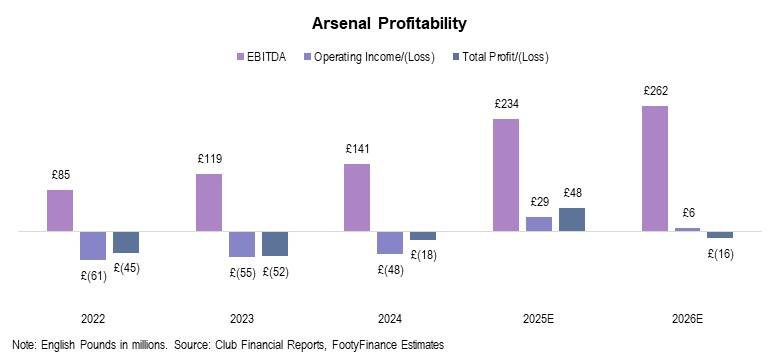

Profitability

Strong EBITDA growth is expected to continue in the 2025/26 season, though operating income and net income are forecasted to decline y/y. Lower operating income levels are primarily driven by expense growth outpacing revenue growth with net income further affected by significantly lower player sale profit vs. the 2024/25 season.

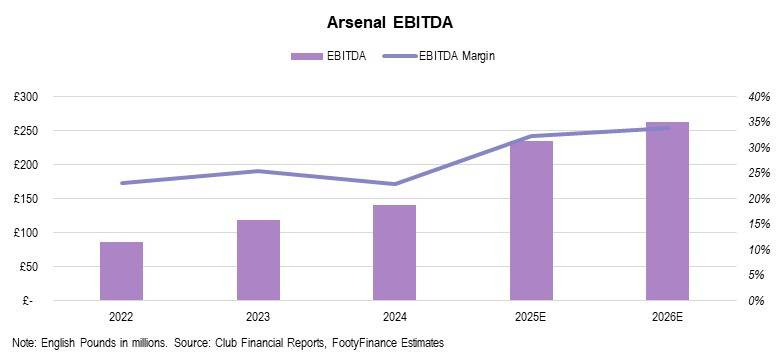

EBITDA

EBITDA margin is expected to modestly expand in the 2025/26 season to 34% (vs. 32% estimate in the 2024/25 season). Compared to average EBITDA margin of 24% for the 2021/22 through 2023/24 seasons, Arsenal continues to show strong EBITDA profitability improvement.

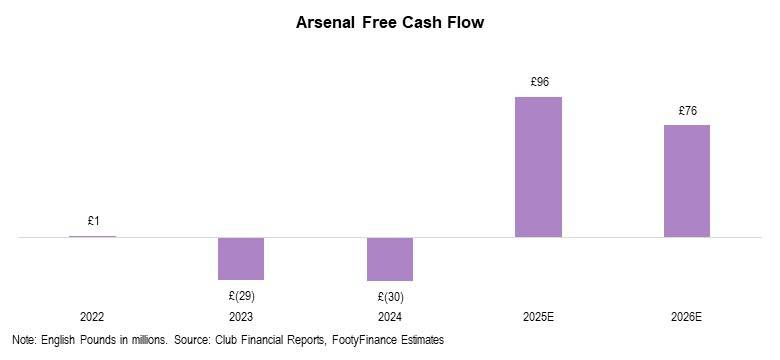

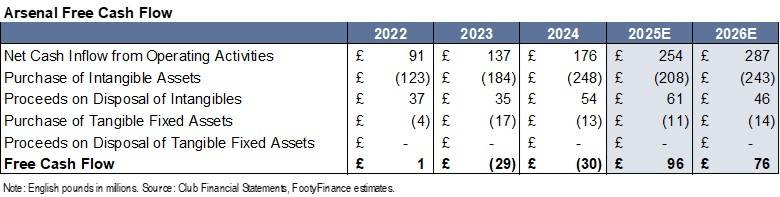

Free Cash Flow

Free Cash Flow is expected to slightly decline in the 2025/26 season, though still remain positive. Current forecasts show Arsenal as the only Big Six club to have positive Free Cash Flow for the 2025/26 season.

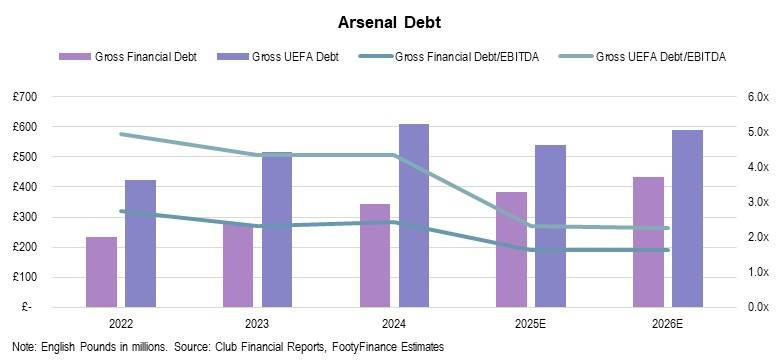

Debt

Gross financial debt balance is expected to come in at £432mm for the 2025/26 season (up from most recently reported figure of £342mm in the 2023/24 season). Leverage increase stems from higher UEFA debt (up from estimated £540mm in the 2024/25 season to £589mm in 2025/26) driven by higher volume 2025 summer transfer window. 2025/26 UEFA debt, however, is down from most recently reported figure of £610mm following the 2023/24 season. Note that Financial Debt includes traditional debt instruments such as owner debt and external loans. UEFA debt adds transfer debt on top of the financial debt figure.

Valuation

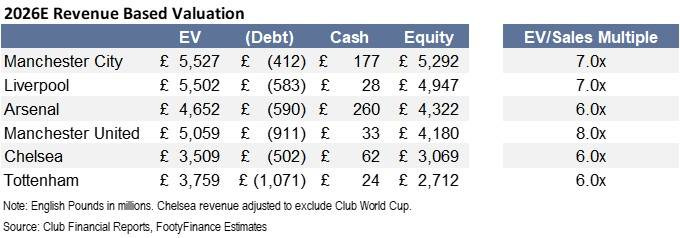

Based on current revenue forecast of £775mm for the 2025/26 season, Arsenal equity is valued at £4.3bn using a 6.0x EV/Sales multiple (in-line with Big Six average per third-party valuations from Forbes, Sportico, and CNBC). While Arsenal has consistently challenged for domestic and European titles in recent years, the club’s multiple should represent a discount to Liverpool and Manchester City, who have been perennial winners over the past decade. Should Arsenal see similar sustained success in the back-half of this decade, then a higher multiple will be justified particularly given the club’s strong revenue growth profile (highest average among Big Six in past five years).

Disclaimer

This report discusses valuation of Arsenal Football Club for informational purposes only and does not constitute investment advice. All investment decisions should be made at one’s own risk and/or with the advice of an investment professional.

This report presents a view only as of the date of this communication and any opinions, estimates, and assumptions expressed herein are made as of the date of this communication. The information contained may be subject to change and/or withdrawal without notice or become incorrect due to passage of time and/or as a result of legal, political, economic, and other changes. FootyFinance does not assume responsibility to notify you of such changes and/or furnish an updated report. FootyFinance does not assume responsibility for results from this model.

FootyFinance is not, by making this material available, providing legal, regulatory, tax, financial, or accounting advice to the recipient of this report or any other party. Sources for the information herein are believed to be reliable, but FootyFinance makes no representation and gives no warranty as to the completeness or accuracy of the information contained herein. Past performance is not indicative of future results. No liability is accepted by FootyFinance for any losses that may arise from any use of or reliance on the information contained herein.